Goldman Sachs Bitcoin ETF Push Signals Wall Street Commitment

Goldman Sachs Group Inc. filed for a Bitcoin ETF on April 14, 2026 – formally entering the issuer side of a market it had previously accessed only as a buyer, and doing so with a product architecture designed specifically for the income-oriented institutional investor, its competitors have largely left underserved.

The filing, submitted under Goldman Sachs ETF Trust as post-effective amendment No. 717 to Form N-1A, proposes the Goldman Sachs Bitcoin Premium Income ETF, an actively managed fund that will hold at least 80% of net assets in Bitcoin-exposed instruments and overlay those positions with call options sold on 40% to 100% of exposure to generate monthly premiums.

The fund will route Bitcoin exposure primarily through existing spot Bitcoin ETPs – principally BlackRock’s IBIT – via a Cayman Islands subsidiary, a structure that allows Goldman to sidestep U.S. commodity restrictions while tapping IBIT’s $55 billion liquidity base.

JUST IN: ⚡️ Goldman Sachs has filed a registration statement with the SEC for a new Bitcoin Premium Income ETF. pic.twitter.com/q7nF2T5dlf

— CoinMarketCap (@CoinMarketCap) April 14, 2026

Portfolio management falls to Goldman Sachs Asset Management’s Raj Garigipati and Oliver Bunn. If the SEC approves it within the standard 75-day window, the fund could launch in late June or early July 2026.

This is not Goldman’s first Bitcoin exposure. It is Goldman’s first attempt to monetize that exposure for clients at scale.

DISCOVER: Best crypto to buy right now – CoinSpeaker’s updated guide

Goldman Sachs Bitcoin Premium Income ETF: Why the Covered-Call Structure Changes the Distribution Equation

Goldman’s entry into the Bitcoin ETF issuer space follows a deliberate accumulation phase. Beginning in late 2024, the firm built $1.57 billion in spot Bitcoin ETF holdings – $1.27 billion in BlackRock’s IBIT and $288 million in Fidelity’s FBTC – representing a 121% quarter-over-quarter increase at the time of disclosure.

By Q4 2025, that position had grown to approximately 13,741 Bitcoin worth $1.71 billion across spot ETFs, alongside $1 billion in Ethereum ETFs, $153 million in XRP ETFs, and $108 million in Solana ETFs per 13F filings. Goldman was learning the market before entering it as a manufacturer.

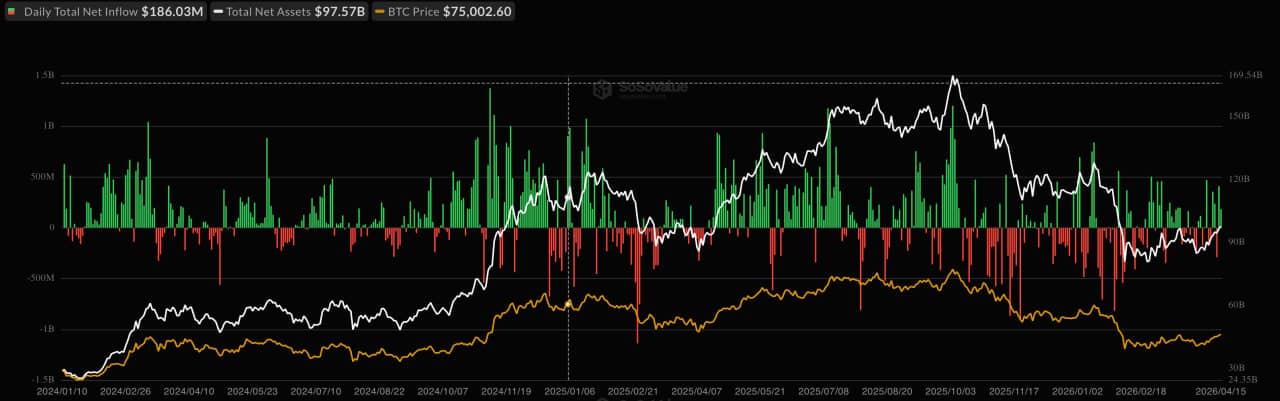

Total Bitcoin Spot ETF Net Inflow / Source: SoSoValue

The covered-call overlay is the mechanistic distinction that matters here. A standard spot Bitcoin ETF delivers full price exposure – gains and losses move in direct proportion to Bitcoin’s price. G

oldman’s product caps that upside during rallies by selling call options against the underlying position, collecting premiums that are then distributed to shareholders as monthly income. The trade-off is explicit: in a strong Bitcoin bull run, the fund will underperform a pure-exposure vehicle. In a sideways or modestly declining market, the premium income cushions returns in a way no spot ETF can replicate.

That framing targets a specific client segment – the wealth management client, the pension allocator, the conservative institutional buyer – for whom Bitcoin’s volatility has historically been the primary barrier to participation.

BlackRock’s comparable BITA ETF employs the same covered-call strategy atop IBIT’s liquidity base, but Goldman’s distribution network gives it a structurally different demand channel. As Arkham Research has described covered-call Bitcoin ETFs, the structure “transforms Bitcoin from a passive asset into an income-generating asset” by harvesting premiums in range-bound conditions – precisely the conditions that cause pure-exposure ETF holders to exit.

Goldman’s wirehouse scale is the variable its competitors cannot easily replicate. The firm’s institutional client base and advisor network represent a distribution pathway that directs capital differently than open-market retail demand – slower to enter, but considerably more durable once committed.

EXPLORE: Best meme coins to watch – CoinSpeaker’s updated rankings

next