Most crypto swap platforms have an identity threshold at some point in the process, such as a KYC trigger buried in the terms, a c...

How to Make Your Crypto Work For You: 4 Different Methods to Explore

Created:  Daniel Francis

Daniel Francis

16 mins

16 mins For most holders, crypto sits in a wallet, doing nothing. But there are smart and relatively safe methods to generate between 5–25%+ APY by putting your assets to work without selling a single coin.

Some methods require nothing more than signing up on a platform and depositing stablecoins, while others demand active position management, on-chain transactions, and a willingness to read a few audits before trusting a protocol with your capital.

Our team explores four of the most trusted approaches, including centralized yield platforms (the easiest and often highest-yielding entry point for most people), native staking, decentralized lending, and liquidity provision on automated market makers.

We explain the differences, point out some of the most credible locations to start earning yield on your crypto, explore risk factors, and walk you through the different methods – from easy mode to hard.

Why Put Your Crypto to Work?

Why Put Your Crypto to Work?

Idle crypto earns nothing, but deployed crypto can compound – and compounding, over time, creates a massive difference between doing something and doing nothing.

Let’s say we have $10,000 in USDC earning 12% APY, compounding monthly. That becomes approximately $12,043 after one year and approximately $17,469 after three years, without touching the principal or making a single additional deposit.

The same $10,000 left alone in a zero-yield wallet is still $10,000, minus whatever inflation has done to its purchasing power.

Method 1: Use a Crypto Yield Platform (Recommended Starting Point)

Centralized finance yield platforms – CeFi, in industry shorthand – work by pooling user deposits together and deploying them into lending markets, structured credit facilities, and other yield-generating strategies. The interest earned then flows back to depositors on a daily or weekly cadence, at rates that have usually run well ahead of those offered by traditional banking.

The process begins with you depositing an asset – Bitcoin, Ethereum, USDT – and the platform allocating it on your behalf. In return, you receive a fixed or variable annual rate, automatically credited to your account. You can withdraw your asset when you need it, subject to whatever lock-up terms you’ve agreed to.

What makes CeFi platforms the natural starting point for most people is simplicity and great rates. There are no gas fees, no private key management, no smart contract approvals, and no impermanent loss to calculate. Interfaces usually look more like a savings dashboard than a DeFi protocol.

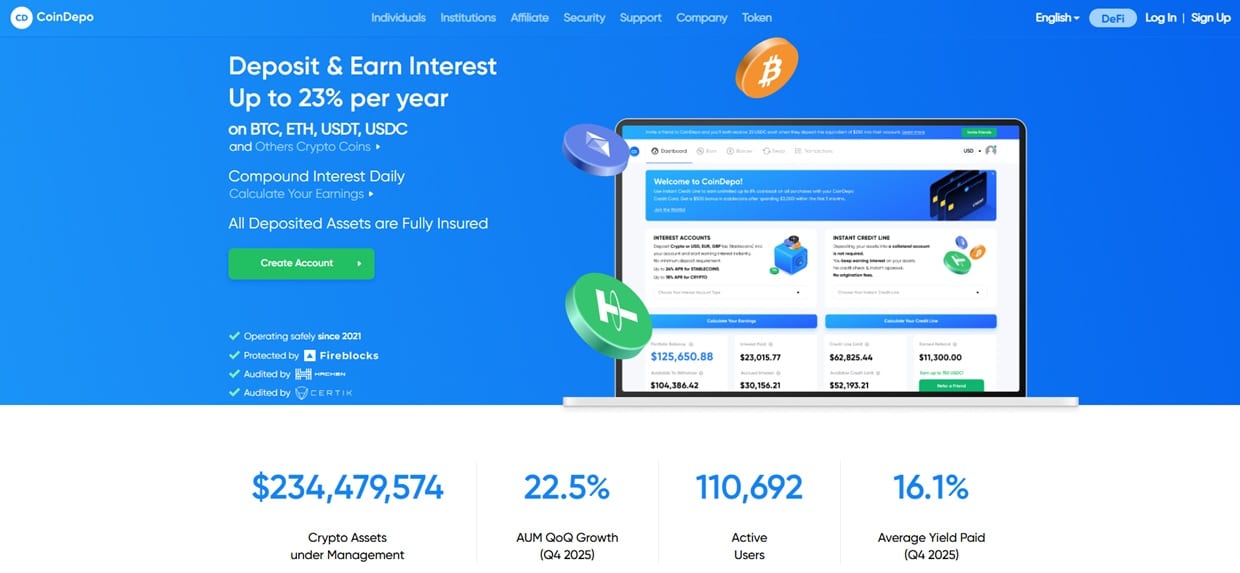

We can examine this through the lens of CoinDepo, one of the most credible options in this space. Founded in 2021, it operates like a structured non-bank financial institution rather than a trading exchange, deploying assets into over-collateralized lending markets and vetted credit channels. As of May 2026, the platform holds $234 million in assets under management (AUM) across 110,000 users.

CoinDepo offers fixed APRs ranging from 12% to 18% on major crypto assets, including Bitcoin, Ethereum, and BNB, that scale with the lock-up duration. Stablecoin yields are higher, running from 17.5% on a weekly basis up to 23% annually on USDT, USDC, and DAI. According to their Q4 2025 report, the average yield per user was 16.1%.

Rates are fixed, not variable, unlike DeFi lending pools, where rates can swing dramatically within hours.

We highlight CoinDepo for its ease of use, safety record, excellent rates, ability to withdraw your assets at any time, and customer-friendly practices (including zero withdrawal fees on crypto assets).

The platform also offers compound interest accounts with automated reinvestment, crypto-backed credit lines, and a “loan without collateral” product in which a user’s deposit serves as collateral but remains active and interest-earning simultaneously.

Pros

- Fixed APRs of 12–23%, some of the most competitive in the CeFi sector

- Zero withdrawal fees

- Institutional custody via Fireblocks MPC

- Regulated in multiple jurisdictions

- Audited by Hacken and CertiK (A rating)

- Flexible terms from weekly to annual

Cons

- Centralized custody – you don’t hold the keys

How to Get Started with CoinDepo

Sign up

Visit coindepo.com and register with your email address or phone number. You’ll receive a verification code to confirm your contact details.

Complete KYC

Full access to yield products requires identity verification. Upload a government-issued ID and complete a facial recognition scan. Approval typically arrives in under 15 minutes.

Deposit your chosen asset

Once verified, select your asset (BTC, ETH, USDT, etc.) and send funds to the unique wallet address provided. Confirm you are sending on the correct network – ERC-20 versus TRC-20, for example – before initiating the transfer.

Open an interest account

Head to the “Earn” tab, create a new account, choose your asset and term length, and confirm. Interest begins accruing immediately. The auto-compound toggle is easy to find and activates automatic reinvestment.

Method 2: Stake Your Cryptocurrency

Staking is the process of locking tokens to participate in a Proof-of-Stake network’s consensus mechanism and earn rewards for helping validate transactions.

Since “the Merge” in September 2022 moved Ethereum from Proof of Work to Proof of Stake, staking allows holders to earn passive income by helping secure the Ethereum network, where validators lock up ETH to earn rewards for proposing and attesting to blocks.

Other major PoS chains – Solana, Cardano, Cosmos – operate on similar principles, each with its own reward rates and lock-up mechanics.

Ethereum staking yield in 2026 hovers between 2–3% APY, with your exact return depending on how you stake. That’s lower than what CeFi platforms offer on the same asset, but the trade-off makes sense: with liquid staking, you’re interacting with a protocol rather than a centralized intermediary.

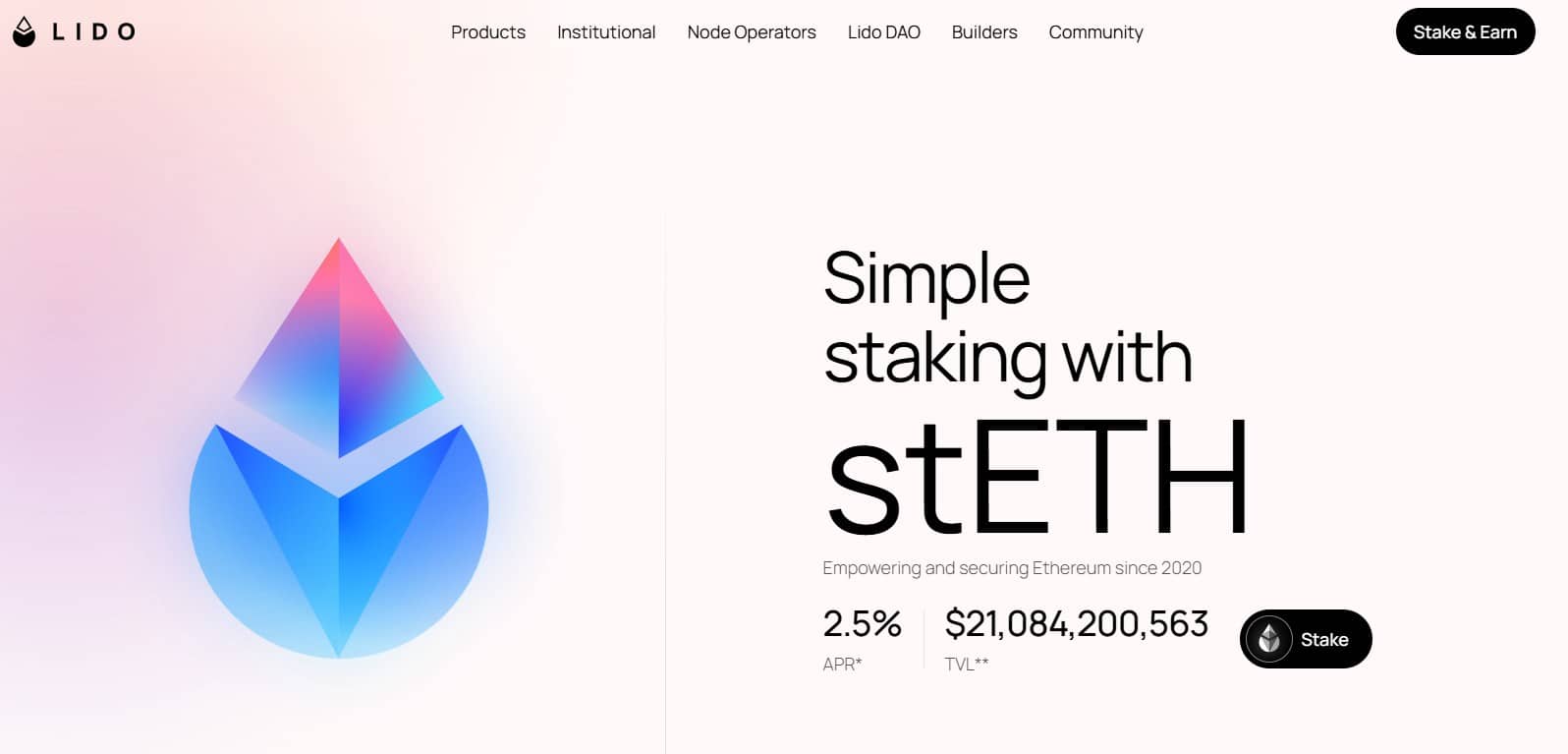

The dominant liquid staking route on Ethereum is Lido, which issues stETH in exchange for deposited ETH. Lido’s flagship product, stETH, delivers a staking APR of ~2.5% after its 10% performance fee is deducted from gross consensus-layer rewards.

As of May 2026, Lido commands over 28% of the Ethereum liquid staking market, with about $25 billion in TVL through stETH. stETH can be used as collateral across Aave, Curve, and most major DeFi protocols, meaning your capital doesn’t sit quietly while it stakes.

Rocket Pool is seen as the darling of the Ethereum community because it is the most decentralized and permissionless protocol. Its APR is 3.5–3.9%, and while the yield is slightly lower than Lido’s for stakers, rETH is considered more tax-efficient in many regions because it appreciates rather than distributing new tokens.

Solo stakers do face slashing risks if they misconfigure their validator, though it is extremely rare with proper setup. Liquid staking adds smart contract risk, and CEX staking introduces counterparty risk. Solana staking through protocols like Jito or directly via Phantom wallet typically yields 5–8% APY on SOL.

Pros

- Directly supports the network

- Liquid staking options (stETH, rETH) maintain token usability in DeFi

- Low operational burden once set up

- rETH’s appreciation model can be more tax-efficient

Cons

- Lower yields than CeFi platforms on the same assets

- Smart contract risk on liquid staking protocols

- Solo staking requires 32 ETH and technical configuration

- Slashing penalties possible, though rare with reputable validators

Method 3: Lend Your Crypto on Lending Protocols

Decentralized lending protocols allow you to supply crypto assets to an on-chain pool, from which borrowers draw liquidity against over-collateralized positions. The interest those borrowers pay flows (proportionally) back to you.

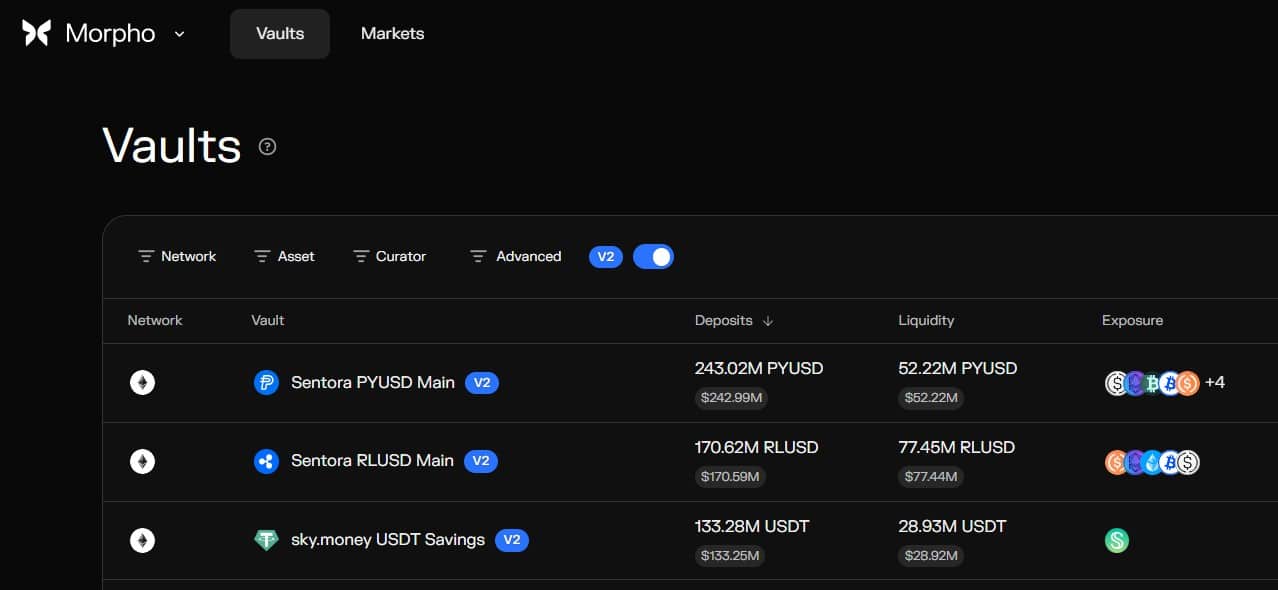

DeFi lending has become massive over the last few years, with on-chain lending capturing roughly two-thirds of the $73.6 billion crypto-collateralized lending market. Aave dominates at $15B+ TVL and $1 trillion in cumulative loans originated, while Morpho is the modular lending layer of choice with $7B+ TVL and an Apollo Global Management partnership.

The rates on offer are real, although variable, with stablecoin supply yields currently ranging from 3–8% APY depending on the protocol and market conditions, which usually outperforms traditional fiat savings (but you do carry smart contract and market risk).

On the more optimized end, Morpho Vaults typically post the highest USDC supply rates (4–8%) because curators actively rebalance across isolated markets to capture the best available rate. Spark SSR offers 4.5–6% on USDS with governance-managed stability, while Aave V3 runs 3–6% with the deepest liquidity.

The workflow won’t suit newbies, but it is still reasonably straightforward – just do your due diligence along the way. Connect a wallet to the protocol, supply the asset you want to lend, and start earning. Most protocols allow withdrawal at any time, though rates fluctuate continuously based on how much of the pool is being borrowed at any given moment. Some protocols also distribute governance tokens as additional yield on top of the base rate.

The risks are worth taking seriously, with smart contract exploits the primary concern – an undiscovered bug in a protocol’s code can result in total loss. Liquidation cascades during sharp market drawdowns can also compress lending rates quickly and, for borrowers, result in forced selling. Rates that look attractive on Monday can be half that by Friday.

For holders considering this path, Compound is a good starting point. It’s a relatively conservative, highly audited, multi-chain option for users who prioritize a long track record over maximizing every basis point.

Pros

- Withdraw from most positions at any time

- Good rate visibility through dashboards like DefiLlama

- Some protocols distribute governance tokens on top of base yield

- Purely non-custodial – your wallet, your keys

Cons

- Smart contract risk is real and non-trivial

- Rates fluctuate, sometimes sharply

- Gas fees for deposits and withdrawals (have $10 in ETH available for gas when using Ethereum mainnet; L2 deployments are far cheaper)

- Liquidation risk if you are also borrowing against your position

Method 4: Provide Liquidity on Decentralized Exchanges

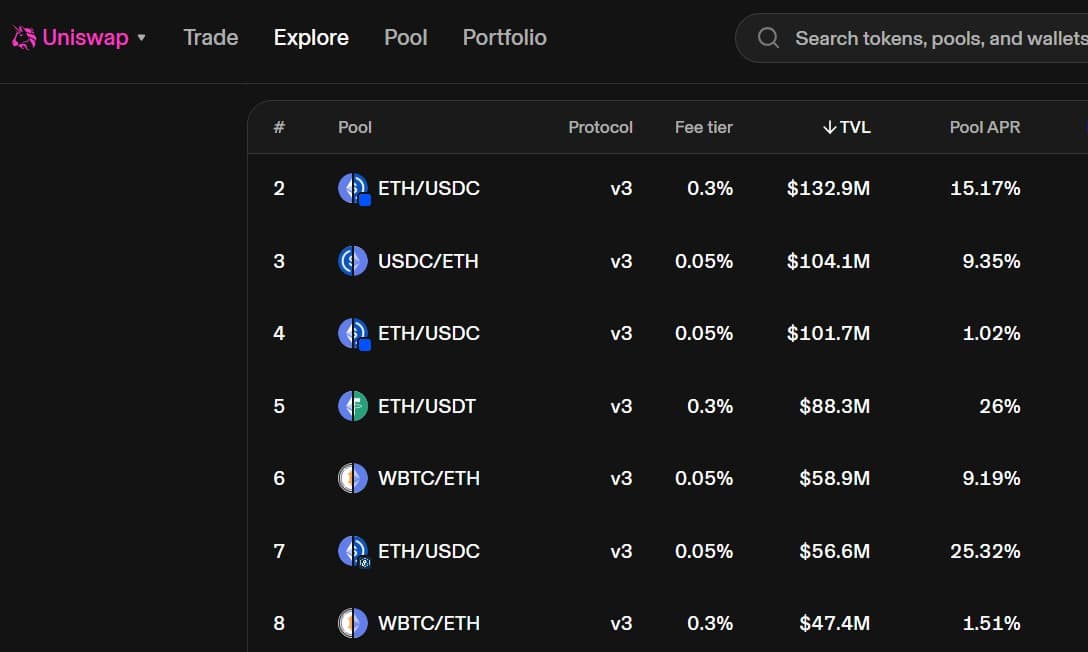

Automated market makers (AMMs) like Uniswap don’t maintain order books; instead, they rely on liquidity providers to deposit token pairs into pools from which traders can swap. In exchange, LPs earn a portion of the fees generated by every trade that passes through their pool, along with any incentive tokens the protocol distributes.

Uniswap v3 was released in May 2021 and introduced concentrated liquidity, allowing LPs to choose specific price ranges rather than providing liquidity across the entire price curve, enabling them to concentrate their capital and deploy it more efficiently. Uniswap v4, released in 2025, reduces network costs for liquidity providers and swappers while introducing more fee tiers and greater customization via hooks, which are smart contract plugins that let developers inject custom logic into liquidity pools.

As of May 2026, over 70% of Uniswap’s daily volume occurs on Layer 2 chains, further reducing the gas costs of managing LP positions.

The yield potential here is the highest of the four methods covered, but so are the complexity and risk. The principal hazard specific to liquidity provision is impermanent loss.

The concept is easier to illustrate than define: if you deposit ETH and USDC into an equal-value pool, and ETH’s price rises sharply, the pool automatically rebalances – selling your ETH as it appreciates. When you withdraw, you end up with more USDC and less ETH than you would have if you’d simply held both. The trading fees you earned in the meantime may or may not offset the gap. This effect is most severe in volatile, asymmetric pairs and less drastic (all things being equal) in stablecoin-to-stablecoin pools.

Mitigation is possible, but requires you to pay really close attention. Stablecoin pairs (USDC/USDT, for example) carry minimal impermanent loss because neither asset moves much relative to the other, and high-volume pools generate more fees, which helps offset IL.

Concentrated liquidity positions (the Uniswap v3/v4 approach) can boost fee yield substantially, but require active range management – if the price moves outside your selected range, you stop earning fees entirely.

Battle-tested platforms like Aave, Compound, Maker, Curve, and Uniswap are the ones to prioritize when deploying on a larger scale.

The process is generally choosing a DEX, connecting your wallet, selecting a pool, and depositing the token pair. Then you receive LP tokens that represent your share, claim fees periodically, and monitor the position’s price range if using concentrated liquidity.

Starting small and on an L2 like Arbitrum or Base keeps transaction costs manageable while you learn.

Pros

- Potentially the highest yields of any method

- Fee income is earned continuously

- No centralized counterparty

- Stablecoin pairs reduce price risk significantly

Cons

- Impermanent loss can exceed fee income in volatile markets

- Concentrated positions require active management

- Smart contract risk

- Gas costs for position management (lower on L2s, but present)

Comparing Crypto Yield Methods

| Method | Ease of Use | Risk Level | Typical APY Range | Liquidity | Best For |

| Yield Platform (e.g. CoinDepo) | Easy | Low | 8–23% | High | Beginners, steady income |

| Staking | Medium | Low–Medium | 2–8%+ | Medium | Long-term PoS holders |

| Lending | Hard | Medium | 3–8%+ | High | Stablecoin fans, DeFi-curious |

| Liquidity Provision | Expert | High | Variable, 10%+ | Medium | Higher risk tolerance |

The choice you make comes down to a few practical factors. If you hold stablecoins and want a predictable yield without on-chain complexity, CoinDepo-style platforms are hard to argue with- the rates are competitive, the mechanics are simple, and the institutional custody structure is a reasonable proxy for security.

If you hold ETH long-term anyway, liquid staking with Lido or Rocket Pool lets the asset work without selling it, at rates that are modest but credible.

Lending on Aave suits those who want DeFi exposure but with more control over exit. Liquidity provision is for people who understand impermanent loss, have time to actively manage positions, and are chasing the top of the yield range.

None of these are mutually exclusive. Many experienced holders run a stablecoin position on a CeFi platform, stake a portion of their ETH, and experiment with one small LP position – that gives you different risk profiles, different time horizons, and lots to learn along the way.

Security Best Practices and Common Mistakes

Security Best Practices and Common Mistakes

The most consistent driver of crypto losses is not market volatility but human error and platform failure.

We strongly recommend using a hardware wallet for any DeFi interaction and enabling two-factor authentication everywhere. Never share your seed phrase – not with a support agent, not with a wallet recovery service, not with anyone. Anyone asking for these is a scammer. Diversify across platforms rather than concentrating your yield-generating assets in one place.

The most common mistakes are predictable: chasing the highest APY without reading what backs it, ignoring the difference between audited and unaudited protocols, failing to claim and reinvest rewards regularly, and over-leveraging borrowing positions that get liquidated in a downturn.

DefiLlama Yields is the essential data aggregator for experienced users hunting for yield across the DeFi landscape. It is not a platform where you deposit funds – it is a neutral, real-time dashboard that scans thousands of yield-generating pools across hundreds of protocols and blockchains. Before deploying into any pool or protocol, check its TVL, 30-day average APY, and audit history. While even a pro will spend a moment daydreaming about triple-digit APYs, when they do exist, they are short-lived opportunities with elevated protocol, liquidity, and strategy risks. Don’t play with them until you’ve earned your wings elsewhere.

Tax Implications

In most jurisdictions, crypto yield is treated as ordinary income when received, whether from staking rewards, lending interest, or LP fees. The moment yield is credited to your account, it is typically treated as a taxable event, valued at the market price at that moment.

Track your cost basis carefully – there are many crypto tax calculators out there. Reward tokens received and later sold will also generate a capital gain or loss in addition to the original income recognition.

Loss harvesting – strategically realizing losses to offset gains – is available in many jurisdictions but requires careful record-keeping to apply correctly.

Crypto tax software (such as Koinly, CoinTracker, TaxBit) can automate much of the transaction-level tracking. For anyone running multiple methods across multiple platforms or who has crypto yield as a major source of income, a crypto-specialist accountant is usually worth the cost.

Conclusion

The ability to hold crypto and make it work has never been easier, with accessible tools, cleaner on-ramps, and real, available yield – even if it comes with caveats that deserve to be taken seriously.

Start with the simplest method. For most people, that means a CoinDepo-style platform – deposit stablecoins, set a term, let it compound, and learn the mechanics before scaling up. Once that feels comfortable, staking native PoS assets is a logical second step. Lending protocols come next. Liquidity provision is the advanced course.

Pick one method, and watch your crypto start working for you. Then stay informed, diversify as you grow, and treat this as a marathon – not a sprint, and not a shortcut.

FAQs

How can I earn passive income from crypto?

What is the easiest way to earn yield on crypto?

Is crypto yield safe?

What is the difference between crypto staking and lending?

What crypto yield method offers the highest APY?

Coinspeaker in Numbers

250K+

Monthly Users

80+

Articles & Guides

5000+

Research Hours

23

Authors

guides

How to Swap Crypto on Godex: A Step-by-Step Guide to No-KYC Crypto Swapping

June 12th, 2026

CoinDepo vs. WhiteBIT Earn Comparison: Yields, Features, Security and More

June 2nd, 2026

Divine Ray (DRC) Price Prediction 2026-2030

June 1st, 2026

In the competitive world of crypto yield generation, CoinDepo and WhiteBIT Earn have built notable reputations as centralized plat...

Although most Web3 social platforms struggle to move beyond the hype phase, Divine Ray has taken a more grounded route. Its team h...

Daniel Francis

, 276 postsDaniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing "information gain" that cuts through market hype to find real-world blockchain utility.