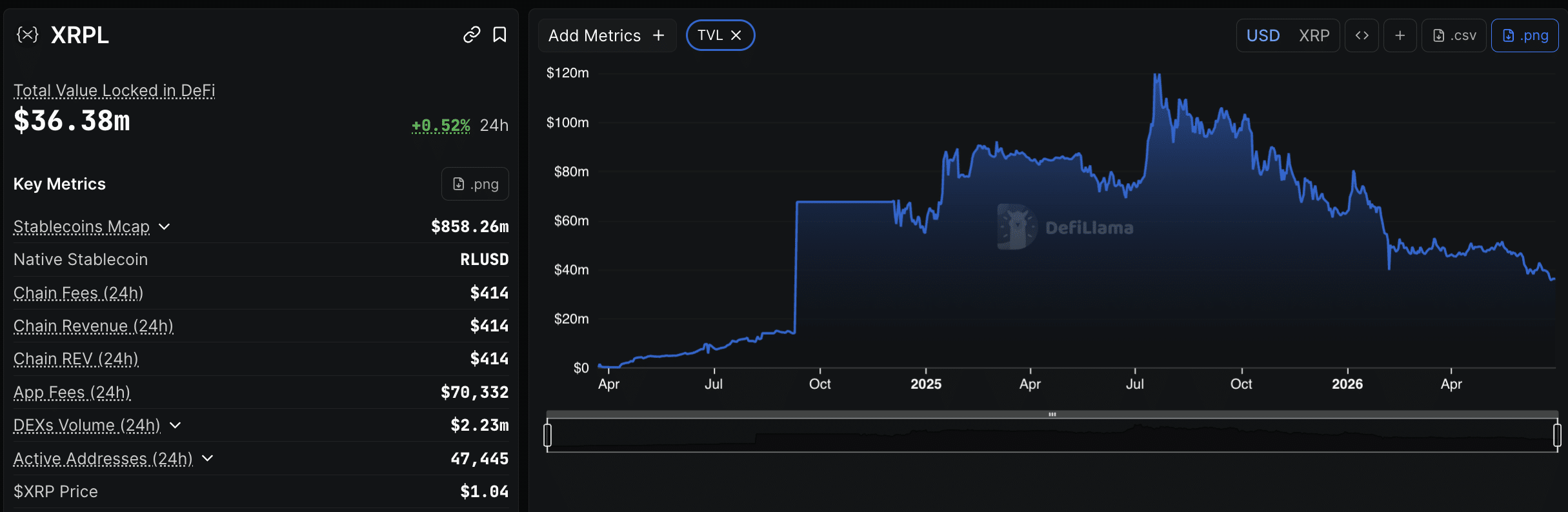

Ripple announced on June 29 that developers can begin testing the XRPL Lending Protocol in a dedicated environment, advancing a dual upgrade comprising two technical specifications, XLS-65 and XLS-66, that would introduce native, fixed-term credit infrastructure directly on the XRP Ledger.

This is pending approval by the network’s validator set under the XRPL amendment process, which requires sustained support of over 80% from trusted validators for two consecutive weeks.

This is not simply another DeFi yield layer grafted onto a blockchain. It is a structural effort to establish the XRP Ledger as a regulated credit rail for institutional participants.

It would require off-chain underwriting authority, first-loss capital protection, and fixed-rate loan terms that map onto bank and asset-manager risk frameworks rather than the automated liquidation logic that governs permissionless protocols.

@Ripple just published the full breakdown of the XRPL Lending Protocol credit infrastructure, natively onchain.

Single Asset Vaults. Standardized loan origination. Repayment and default logic enforced at the protocol layer.

XRPL Lending Protocol: How the Dual Upgrade Is Structured

The mechanism functions as follows: XLS-65 establishes the Single Asset Vault, a standardized pooling format that allows liquidity providers to deposit one asset type, such as XRP or RLUSD, and earn yield.

XLS-66, the Lending Protocol layer, governs loan terms, repayment schedules, interest calculations, and default conditions, all of which are enforced at the protocol level rather than through external smart contracts.

Loans under the design are fixed-term and uncollateralized, a deliberate departure from collateral-dependent models such as Aave. Creditworthiness assessment remains off-chain, preserving institutional control over lending decisions while on-chain logic handles lifecycle events once a loan is originated.

Losses from defaults are absorbed first by pool managers and underwriters – a first-loss capital structure that mirrors tranched credit in traditional finance.

Ripple said the design choice reflects deliberate architecture rather than a limitation. “This separation mirrors real financial infrastructure,” the company stated. “By preserving that distinction, XRPL can support a wider range of credit structures over time, rather than hard-coding one lending model into a single application.”

RippleX developer Edward Hennis has described the target as “real credit, not a DeFi gambling pool,” characterizing the system as regulation-friendly institutional DeFi with loan durations typically running 30 to 180 days at fixed rates.

All you have to do is spot and chill.

As we progress into H2 2026 we are likely to witness more historical oversold signals print for $XRP, such as the 2W RSI reaching its lowest levels of 34

Higher lows or lower lows under lower highs: all led to major breakouts eventually 🚀 pic.twitter.com/6N7WSYUwcp

On-Chain Credit Context: RWAs, RLUSD, and the Ondo Precedent

Ripple frames the lending protocol as the functional complement to tokenized RWA activity already occurring on XRPL. In May 2026, Ondo Finance executed the first cross-border, cross-bank redemption of tokenized US Treasuries on the ledger, a milestone Ripple described as proof that moving an asset on-chain is only half the infrastructure problem.

The XRPL Lending Protocol, if activated, would allow those same tokenized assets to serve as working capital rather than static inventory, providing payment providers short-duration liquidity and enabling treasury teams to generate revenue by lending digital assets under predefined terms.

RLUSD, Ripple’s stablecoin, is positioned as a primary vault asset within that credit structure. According to CoinGecko, RLUSD has reached a $1.5Bn market cap since its late-2024 debut, giving the lending vaults a liquid, dollar-denominated base asset with meaningful existing supply. The protocol’s activation would deepen RLUSD’s on-chain utility beyond payments and into on-chain credit markets.

Validator Vote and Ripple Price at Time of Announcement

The amendment entered validator voting following the XRPL v3.1.0 release in January 2026, according to multiple reports. As of the June 29 announcement, the vote has not concluded.

RippleX has applied formal verification to the XLS-65/66 code and is offering up to $200,000 in security bounties to researchers who can identify flaws in the lending protocol’s design or implementation before any mainnet activation.

XRP traded around $1.05 at the time of the announcement, down -8% over the prior week. The token had fallen to its lowest level since President Donald Trump’s reelection the previous Thursday, briefly nearing $0.99 in sympathy with Bitcoin’s movement.

The analytical question is no longer whether XRPL can move assets on-chain; it is whether the validator set will ratify the credit infrastructure needed to put those assets to work.

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing "information gain" that cuts through market hype to find real-world blockchain utility.