Circle, the issuer of the USDC stablecoin, has unveiled cirBTC, a new Bitcoin-backed token designed to bring the world’s largest digital asset into decentralized finance applications – including lending, borrowing, and liquidity protocols – by addressing the trust deficit that has constrained competing wrapped Bitcoin products.

The token is set to launch on Ethereum and Circle’s own Arc blockchain, with additional chain integrations expected in the coming months. The announcement marks Circle’s most direct entry into Bitcoin infrastructure to date, extending a product portfolio that previously centered on dollar-denominated stablecoins and tokenized money market instruments.

Circle Wrapped Bitcoin is coming.

Backed 1:1 by BTC and readily verifiable onchain, cirBTC is being built to work seamlessly with Circle infrastructure and the broader DeFi ecosystem.

Circle CEO and co-founder Jeremy Allaire framed the launch explicitly as an infrastructure play rather than a speculative product. In a post on X, Allaire stated that Circle is “bringing the same infra that supports USDC, EURC, and USYC to the largest digital asset, creating a neutral infrastructure for new applications for on-chain BTC.” That framing – neutral infrastructure – is doing significant argumentative work: it positions cirBTC not as a yield product Circle controls, but as a settlement layer Circle operates.

Rachel Mayer, Circle’s VP of Product, offered the sharpest diagnosis of the problem cirBTC is designed to solve. “Bitcoin is sitting on the sidelines of DeFi,” Mayer said in a post on X. “Not because people don’t want yield or liquidity – it’s because they don’t trust the wrapper.” That sentence encapsulates the structural case for a new entrant: the problem is not demand, it is counterparty risk perception.

cirBTC Circle Bitcoin Mechanics: What the Token Is and How It Works

cirBTC is a wrapped Bitcoin token – Bitcoin held in custody and represented as an ERC-compatible token on-chain – but Circle is differentiating it from existing products primarily through custodial architecture and issuer credibility.

The token operates on Ethereum and Arc, Circle’s stablecoin-optimized Layer 2 network that the company has been developing since 2024, with the Arc environment designed to support gas-free transactions through a combination of native USDC fee settlement, a developer-sponsored “Gas Station” model, and a “Paymaster” system enabling USDC-denominated gas on external chains including Ethereum, Polygon, and Solana.

$1.7T of bitcoin is sitting on the sidelines of DeFi. Not because people don't want yield or liquidity, it's because they don't trust the wrapper.

cirBTC is Circle's answer: 1:1 backed, onchain-verifiable, and built on infrastructure the market already trusts.

The technical implication is that cirBTC holders interacting within Arc-native protocols will not require ETH or any separate gas token to execute transactions – a friction point that has historically discouraged retail and institutional participation in wrapped asset DeFi. Circle’s gas-free developer toolkit, released in March 2026, provides the underlying plumbing that makes this viable at the application layer.

cirBTC is not a yield-bearing instrument by design; it is a liquidity representation of Bitcoin intended to be deployed into external yield strategies by holders or protocols. This distinguishes it structurally from Circle’s USYC – a tokenized money market fund enabling 24/7 USDC redemptions – which generates returns within Circle’s own product stack. cirBTC’s yield, if any, flows from wherever it is deployed.

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing "information gain" that cuts through market hype to find real-world blockchain utility.

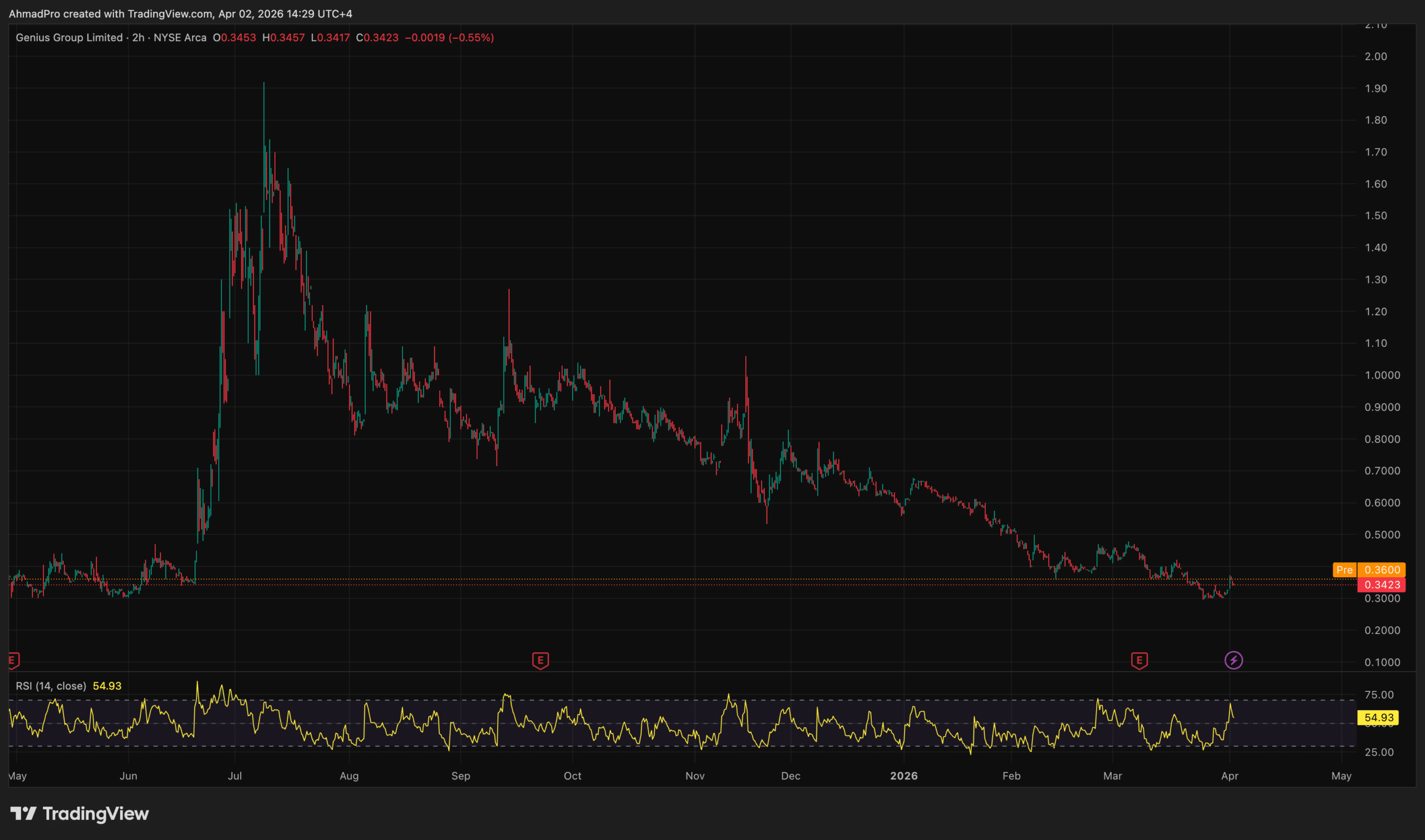

Genius Group (GNS) liquidated its entire Bitcoin treasury – 84 BTC valued at approximately $5.7 million as of March 2026 – to retire $8.5 million in debt, a full disposition that confirms the company’s balance sheet had reached a point where no alternative capital source was available to service the obligation.

The sale was disclosed alongside the company’s Q1 2026 earnings release and represents a complete reversal of the Bitcoin accumulation posture the company publicly committed to just eighteen months ago.

The liquidation is particularly notable given that Genius Group’s “Bitcoin first” strategy, announced in November 2024, pledged to allocate 90% or more of current and future reserves to Bitcoin. That the company exited its entire position to satisfy an $8.5 million debt – a figure smaller than its peak treasury valuation – is evidence of a funding model that lacked the structural redundancy to survive a sustained drawdown without forced asset sales.

Genius Group sells all Bitcoin reserves to repay $8.5M debt. 👀

Genius Group Bitcoin Sale: What the Full Liquidation Reveals

By the time Genius Group entered Q1 2026, its holdings had already contracted sharply from peak levels. The company had accumulated 440 BTC at a total cost basis of approximately $42 million – an average acquisition price of roughly $95,519 per BTC – according to disclosures made in early 2025.

The 84 BTC remaining at the time of the full liquidation implies the company had sold roughly 356 BTC across the preceding twelve months, largely under operational and legal duress rather than as a deliberate strategic exit.

At an $5.7 million market value for 84 BTC, the implied exit price on the final tranche was approximately $67,857 per coin – well below the $95,519 average cost basis on the full position. That spread represents a meaningful realized loss on at least the portion of the portfolio acquired near peak prices, though Genius Group has not disclosed a precise per-tranche cost basis or execution venue for the Q1 2026 sale.

The company’s press release attributed the proceeds to full repayment of its $8.5 million debt obligation, with Genius Group simultaneously restructuring its broader debt agreement framework alongside the liquidation.

The $8.5 million debt figure is itself a diagnostic data point. At Genius Group’s current scale – Q1 2026 revenue of $3.3 million, up 171% year-on-year – the obligation represented more than two full quarters of revenue, leaving the company with no credible path to service the debt organically without asset liquidation. The Bitcoin treasury, originally framed as a strategic reserve, functioned in practice as the lender of last resort.

Balance Sheet Pressure and What the Liquidation Reveals About Smaller Treasury Operators

The structural failure mode here is straightforward: Genius Group attempted to replicate a Bitcoin treasury strategy designed for companies with access to deep equity and debt capital markets, without the balance sheet size or market capitalization to absorb a sustained BTC price decline.

At peak in early 2025, the company’s 440 BTC position was worth approximately $46 million against a market capitalization of $33.1 million – a leverage ratio that left no margin for drawdown once the equity premium collapsed and the legal injunction from the U.S. District Court for the Southern District of New York blocked further capital raises and Bitcoin purchases in April 2025.

That court order – a temporary restraining order and preliminary injunction that barred Genius Group from selling shares or using investor funds to buy Bitcoin – is the proximate cause of the treasury’s decline, forcing the company to draw down holdings to fund operations rather than accumulate through the dip.

The share price fell 53% within six weeks of the injunction, compressing the equity premium that smaller Bitcoin treasury firms depend on to fund acquisition cycles. Without that premium, the accumulation flywheel stops.

GameStop’s retention of its full 4,710 BTC position through comparable market pressure illustrates the distinction: companies with unencumbered cash reserves and no covenant exposure can hold passively; companies running thin on liquidity cannot.

The contrast with Michael Saylor’s Strategy – which has continued accumulating through the same bear market conditions that pressured Genius Group into full liquidation – is not merely narrative. It is structural. Strategy’s model is designed around perpetual capital access; Genius Group’s was not, and the gap between those two designs became the entire story.

Genius Group stated it intends to rebuild its Bitcoin treasury “when it believes market conditions are more favorable.” The next material test of that commitment will arrive with Q2 2026 earnings – specifically, whether the company, now debt-free, begins deploying capital back into Bitcoin or whether the operational constraints that produced the liquidation prove more durable than the strategy that preceded them.

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing "information gain" that cuts through market hype to find real-world blockchain utility.

The New Hampshire Business Finance Authority (BFA) is set to issue $100 million in Bitcoin-collateralized bonds carrying a provisional Ba2 rating from Moody’s Investors Service – a speculative-grade designation that places this instrument two notches below the lowest investment-grade threshold and marks the first known instance of a U.S. public authority issuing debt fully backed by Bitcoin.

For municipal bond markets accustomed to state-level paper rated Aa or above, a Ba2 on a crypto-collateralized structure is not merely a footnote – it is a signal that the conventional muni buyer universe is, by mandate, largely excluded before the first coupon is cut.

🚨NEW HAMPSHIRE TO ISSUE FIRST RATED BITCOIN-BACKED BOND

The New Hampshire Business Finance Authority plans to issue what appears to be the first Moody’s-rated Bitcoin-backed bond (Ba2).

The bond is backed by BTC held with BitGo and does not put state public funds at risk. pic.twitter.com/svYLhbtIXp

We suspect the rating’s practical effect is more consequential than its headline suggests. Ba2 paper cannot be held by most municipal bond funds, pension systems operating under fiduciary investment-grade floors, or insurance company general accounts subject to NAIC capital charge rules – meaning the natural buyers here are high-yield muni investors, hedge funds, and crypto-native fixed-income allocators, a materially different compliance posture than any prior New Hampshire public authority issuance.

BFA Bond Structure: Bitcoin Collateral, Limited Recourse, and the CleanSpark Connection

The bonds will be issued in two series – Series 2026A-1 and Series 2026A-2, both maturing in 2029 – with individual class balances not yet publicly disclosed, per Moody’s Tuesday statement. Series 2026A-2 holders are entitled to optional additional payments at maturity if Bitcoin appreciates sufficiently after principal, interest, and expenses are covered – a feature that introduces asymmetric upside exposure uncommon in conventional fixed-income structures.

The underlying borrower is NH Cleanspark Borrower Trust 2026-1, an entity linked to CleanSpark, a publicly traded Bitcoin mining firm, which posts Bitcoin as the loan collateral. BitGo Bank & Trust will serve as custodian, holding the BTC in segregated wallets, and will also act as liquidation agent – responsible for converting Bitcoin into cash to service interest and principal payments as they come due.

Crucially, the bonds are structured as limited recourse obligations, payable solely from proceeds of the Bitcoin collateral. No public funds backstop the debt. The BFA acts as lender in the underlying loan structure but carries no general obligation liability, which insulates New Hampshire taxpayers from any shortfall – though it also removes the implicit state credit support that typically underpins quasi-public authority paper.

The collateral arrangement launches at a 1.60x coverage ratio – meaning Bitcoin holdings must be worth 1.60 times the outstanding loan balance at inception. A mandatory full redemption of the bonds is triggered if that ratio deteriorates to 1.40x.

Moody’s applied a 72.06% advance rate in its analysis, factoring in Bitcoin’s price volatility and the assumption of a two-day liquidation exposure window – the period during which BitGo would be unwinding BTC positions into market depth before full settlement could occur.

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Neil is a professional cryptocurrency content writer with years of experience. He has written for various cryptocurrency websites to report on breaking news, and been hired by all sorts of cryptocurrency projects, to create content that would increase their exposure and attract more potential investors.

A new paper from Google Quantum AI has compressed the estimated hardware requirements for breaking elliptic-curve cryptography – the signature scheme underpinning Bitcoin and crypto transactions – by roughly 20-fold, moving a long-running theoretical threat measurably closer to an engineering problem.

The research, co-authored by Google researchers, Ethereum Foundation researcher Justin Drake, and Stanford cryptographer Dan Boneh, revises the physical qubit threshold downward from prior estimates exceeding 10 million to fewer than 500,000, a compression that forces institutional risk models to treat Q-Day as a medium-term rather than generational concern. At current market prices, the assets directly exposed to the cryptographic assumption at issue exceed $600 billion across Bitcoin, Ethereum, and stablecoins.

Shor’s Algorithm Efficiency: What the 20x Qubit Compression Actually Represents

The operative mechanism here is Shor’s algorithm applied to the 256-bit elliptic curve discrete logarithm problem – the mathematical foundation of ECDSA (Elliptic Curve Digital Signature Algorithm), which Bitcoin and Ethereum use to authorize transactions by proving private key ownership without revealing the key itself.

A sufficiently capable quantum computer running Shor’s algorithm could, in principle, derive a private key from an exposed public key, allowing an attacker to sign transactions and drain funds without authorization.

Prior estimates, drawn from analyses between 2017 and 2023, projected that executing this attack would require machines on the order of millions of physical qubits – hardware so distant from current capability that the threat horizon sat comfortably in the 2040s under most institutional models.

Many are wondering "what Google saw" that caused them to revise their post-quantum cryptography transition deadline to 2029 last week. It was this: https://t.co/dQtmTK9pdz

The Google Quantum AI whitepaper, published March 30, 2026, revises that threshold sharply: Shor’s algorithm for the same problem can now be executed with no more than 1,200 logical qubits and 90 million Toffoli gates – or alternatively 1,450 logical qubits and 70 million Toffoli gates – on a superconducting, cryptographically relevant quantum computer (CRQC) with fewer than 500,000 physical qubits, completing the attack in minutes from a primed state.

The distinction between logical and physical qubits matters: physical qubits are noisy and require error-correction overhead, meaning many physical qubits are needed to sustain one reliable logical qubit. The 20x compression reflects advances in error-correction efficiency and gate optimization – not a new algorithmic breakthrough, but a tighter engineering implementation of a known approach. Google does not claim such a machine exists today. The paper’s significance is in recalibrating what the hardware target looks like, not in announcing it has been reached.

Bitcoin Crypto Address Exposure: Which Outputs Are Vulnerable to Quantum and How Much BTC Is at Risk

Bitcoin’s cryptographic exposure is not uniform across all address types. The highest-risk category is pay-to-public-key (P2PK) outputs – legacy address formats, prevalent in early Bitcoin blocks, including Satoshi-era coinbase outputs, where the full public key is written directly into the blockchain and permanently visible.

A quantum attacker with a functional CRQC could target these addresses without needing to observe a live transaction, since the public key is already on-chain.

A secondary category involves address reuse in pay-to-public-key-hash (P2PKH) outputs: once a user spends from a P2PKH address, the public key is revealed in the transaction, creating a window – however narrow – during which a CRQC could theoretically derive the private key before the transaction confirms.

Approximately 6.7 million Bitcoin addresses currently carry exposed public keys through one of these two mechanisms, representing a material share of the circulating supply. Whether any of those addresses belong to sophisticated institutional holders is unknown publicly, but the concentration of early-mined Bitcoin in P2PK outputs means the aggregate BTC-at-risk figure is not trivial.

Saw some people panicking or asking about quantum computing's impact on crypto. At a high level, all crypto has to do is to upgrade to Quantum-Resistant (Post-Quantum) Algorithms. So, no need to panic. 😂

In practice, there are some execution considerations. It's hard to…

The Bitcoin protocol has no active post-quantum upgrade path at the consensus level. Discussions around quantum-resistant signature schemes – including lattice-based alternatives being standardized by NIST – exist in developer forums, but no Bitcoin Improvement Proposal has reached consensus-stage consideration for a post-quantum migration.

The compressed timeline Google has published changes the urgency calculus for that discussion, even if the engineering problem of migrating a UTXO set of this scale remains formidable.

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing "information gain" that cuts through market hype to find real-world blockchain utility.

Senators Bill Cassidy and Cynthia Lummis introduced the Mined in America Act on March 30, 2026, a bill that would establish a voluntary federal certification program for domestic Bitcoin mining facilities, codify the Strategic Bitcoin Reserve into statute, and create a direct Treasury procurement channel through which certified miners sell newly mined BTC to the federal government in exchange for a capital gains tax exemption.

The legislation, which carries no new fiscal authorizations, designates the Department of Commerce as the administering certifying body and directs the National Institute of Standards and Technology and the Manufacturing Extension Partnership to support domestic mining hardware development – a mandate that implicitly acknowledges what the bill’s sponsors describe as an untenable dependence on hardware manufactured by foreign adversaries.

The bill now awaits committee referral, with the Senate Commerce, Science, and Transportation Committee the most likely venue for initial review. It arrives as a companion to the broader reserve architecture that Senator Lummis has advanced since her introduction of the BITCOIN Act of 2025, which first proposed Treasury-managed custody of federal Bitcoin holdings.

We suspect the more consequential provision is not the certification label itself but the Treasury procurement mechanism – a structure that, if enacted, would make the federal government a recurring, price-insensitive buyer of domestically mined BTC, introducing a demand floor with no clear precedent in sovereign commodity acquisition.

Mined in America Act: Legislative Mechanics and Operative Provisions

The mechanism functions as follows: a mining facility or pool applying for “Mined in America” certification must demonstrate to the Department of Commerce that it operates no equipment manufactured by entities domiciled in, or controlled by, countries designated as foreign adversaries under existing U.S. trade law – a category that presently encompasses China, Russia, Iran, North Korea, Cuba, and Venezuela.

Full hardware phase-out is required by the end of the decade, giving operators a defined transition runway but imposing a hard deadline on continued use of equipment from manufacturers such as Bitmain Technologies and MicroBT, which together account for the overwhelming majority of the approximately 97% of mining rigs currently sourced from Chinese-domiciled companies.

Senators Cynthia Lummis and Bill Cassidy just introduced the "Mined in America Act." This one is worth paying attention to.

The problem it addresses is straightforward. The United States controls roughly 38% of the global Bitcoin hash rate, but the vast majority of the hardware… pic.twitter.com/7LF4kO6rO0

Certified operators gain access to pre-existing Department of Energy and U.S. Department of Agriculture program benefits – including grid stabilization contracts, renewable energy absorption arrangements, and methane capture initiatives at landfill and oil field sites – without triggering new appropriations. That framing is notable because it allows sponsors to characterize the bill as fiscally neutral while still delivering material economic incentives to compliant miners.

The reserve codification provision links certification directly to Treasury acquisition: miners holding the “Mined in America” designation may sell newly mined Bitcoin to the Treasury at market rates in exchange for exemption from capital gains tax on the transaction. Revenue from staking rewards and airdrop income on the government’s existing seized-asset holdings – estimated between 198,000 and 328,000 BTC following Trump’s 2025 executive order – would fund further open-market purchases, creating a self-reinforcing accumulation structure that requires no direct congressional appropriation beyond the initial statutory authorization.

Bitcoin Mining Nationalization: Hash Rate Distribution and BTC Supply Implications

The transmission chain operates as follows: the certification regime, combined with the tax exemption incentive, creates a structural tilt toward domestic hardware procurement that – if adopted at scale – would concentrate an increasing share of U.S. hash rate among operators whose capital expenditure cycles are now tied to a nascent domestic ASIC manufacturing base rather than the established Bitmain and MicroBT supply chains.

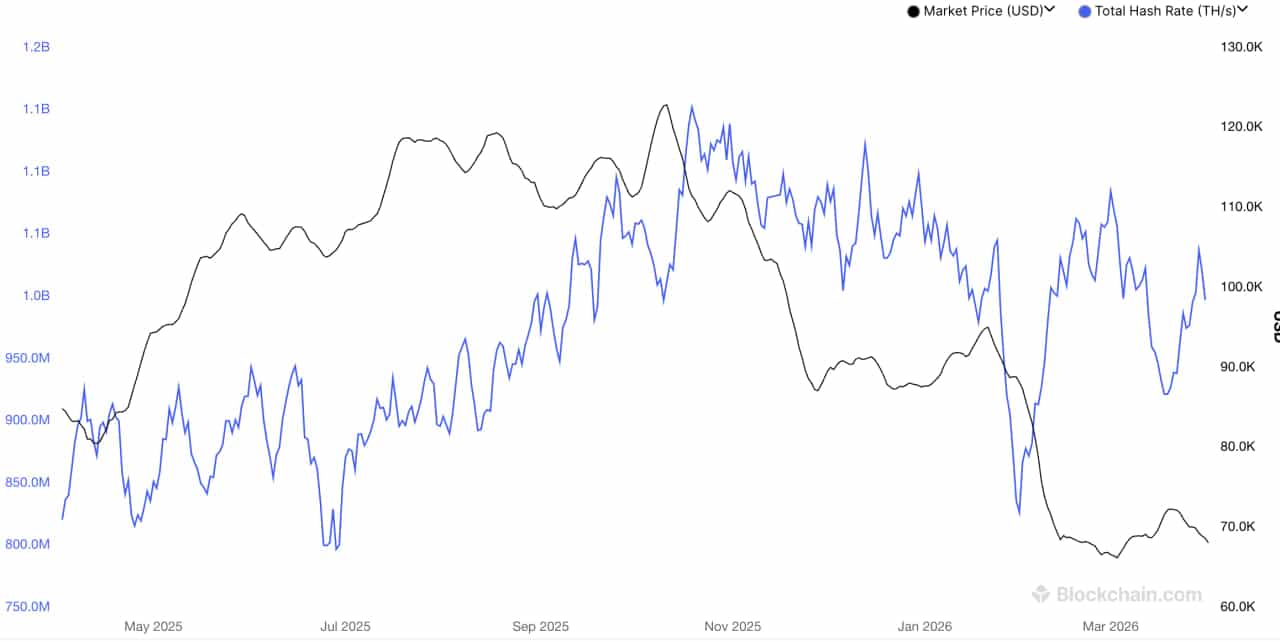

The United States currently controls approximately 38% of global Bitcoin hash rate, a figure that makes it the dominant single-jurisdiction contributor to network security, yet one achieved almost entirely on imported hardware whose firmware integrity has already been called into question by late 2024 U.S. Customs inspections that identified remote-access vulnerabilities in imported Chinese mining rigs.

We anticipate that the near-term hardware transition cost – sourcing certified equipment from a domestic manufacturing base that does not yet exist at commercial scale – will compress margins for mid-tier miners who lack the capital to absorb dual procurement cycles, potentially accelerating consolidation toward larger, better-capitalized operators who can participate in the Treasury sales program. The parallel to the post-2021 China mining ban is instructive but imperfect: that episode redistributed hash rate geographically without altering the hardware supply chain; the Mined in America Act, if enacted, targets the supply chain itself.

On the supply side, the Treasury procurement channel introduces a buyer whose acquisition behavior is not governed by profit motive – a structural novelty in Bitcoin’s market history. We suspect the effective float of newly mined BTC available to secondary markets would narrow if a meaningful share of certified mining output is routed directly to the reserve, a dynamic with directional implications for spot supply that analysts have not yet fully priced into hash-rate-adjusted valuation models.

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing "information gain" that cuts through market hype to find real-world blockchain utility.

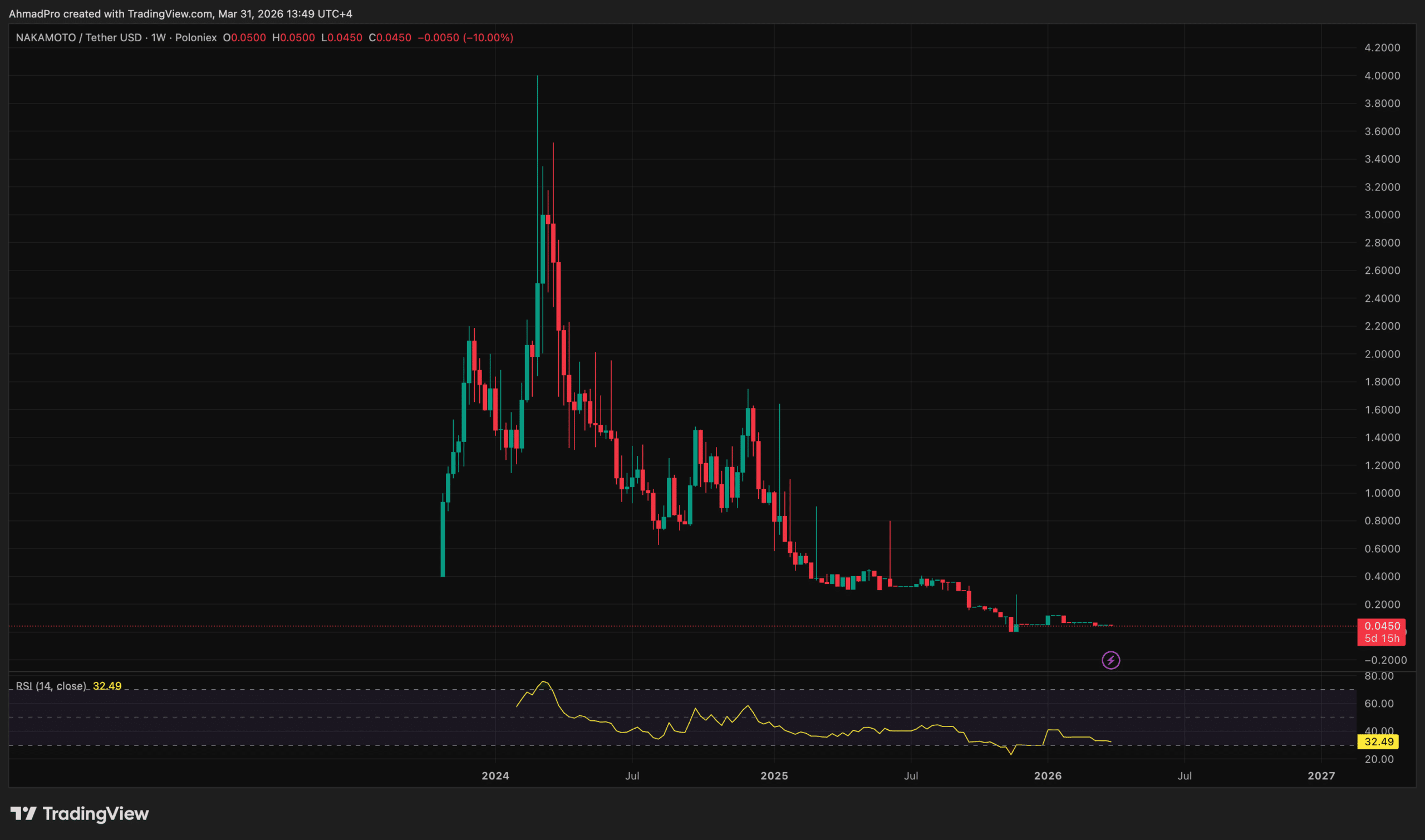

Nakamoto Holdings, the Bitcoin-native conglomerate founded by BTC Inc. CEO David Bailey, sold approximately $20 million worth of Bitcoin at a realized loss of roughly 40%, a liquidation event that implies an average acquisition cost somewhere in the range of $33,000 per BTC against a sale price consistent with market levels at the time of execution.

The transaction was not framed as a routine portfolio rebalancing; a 40% realized loss on a position of this size, for a firm whose entire strategic identity is built around BTC accumulation, signals a forced or at minimum urgency-driven disposition.

For a company that raised over $750 million in mid-2025 explicitly to seed and hold Bitcoin treasury positions globally, selling at a deep loss raises direct questions about liquidity management and the durability of its funding model.

Bitcoin treasury company Nakamoto Inc. (NASDAQ: NAKA) disclosed in its 10-K filed on March 30, 2026, that it sold approximately 284 BTC in March for about $20 million, with an average selling price of around $70,422 per BTC. In 2025, the company net purchased 5,342 BTC with a… pic.twitter.com/DRq8cpT0L6

Nakamoto merged with healthcare provider KindlyMD in May 2025, securing a record $510 million PIPE alongside additional debt financing, with Anchorage Digital handling custody. The architecture was designed to cycle BTC gains back into accumulation while maintaining a 40% public equity exposure cap – a structure that, in theory, insulates the BTC stack from forced liquidation. A $20 million sale at a 40% loss suggests the architecture is under pressure it was not designed to absorb.

Implied Acquisition Cost vs. Realized Exit Price For Nakamoto Bitcoin Holdings

Working from the reported figures, a 40% realized loss on a $20 million sale implies the position was carried at a cost basis of approximately $33.3 million – meaning Nakamoto effectively recovered $0.60 on every dollar deployed into that tranche of Bitcoin.

If the sale occurred at Bitcoin prices in the $80,000–$95,000 range that characterized much of early-to-mid 2026, the implied acquisition price for this specific tranche would place the original purchase somewhere between $133,000 and $158,000 per coin – levels consistent with late-2025 peak accumulation when treasury firms were competing aggressively for spot supply.

The precise vehicle for the sale – whether OTC block, open-market execution, or exchange liquidation – has not been confirmed, and the on-chain footprint has not been independently verified by Arkham Intelligence or Lookonchain at time of writing.

What the math clearly confirms: this was not a tax-loss harvest on a marginal position. A $13.3 million realized loss represents a meaningful destruction of capital for a firm that positioned itself as a long-duration BTC holder, not a trading entity. The numbers crystallize a core structural vulnerability – acquiring BTC near cycle highs with leveraged or equity-dilutive capital leaves no margin for drawdown without eventual forced realization.

Balance Sheet Pressure and What the Liquidation Reveals

Nakamoto’s funding model depends on mNAV arbitrage: issue equity or notes at a premium to net asset value, deploy proceeds into BTC, and let appreciation widen the spread. That engine runs in reverse when the stock collapses.

By early 2026, Nakamoto’s share price had fallen roughly 99% from its May 2025 peaks, effectively closing off the ATM and PIPE channels that provided its accumulation fuel. With equity-based financing unavailable at viable dilution rates, the firm’s options narrow to debt service from cash reserves or liquidation of BTC holdings – the latter being precisely what this transaction appears to represent.

GameStop, by contrast, retained its 4,710 BTC position despite external speculation about a sell-off – a posture only sustainable for firms without acute debt service obligations. Nakamoto’s realized loss suggests it has neither the premium engine nor the unencumbered balance sheet to absorb the drawdown passively.

Governance risk compounds the balance sheet stress. Nakamoto’s concurrent acquisition of Bailey-owned BTC Inc. and UTXO Management – using shares valued near $1.12 each following the 99% collapse – has drawn criticism from market watchers who characterize the moves as self-dealing at shareholder expense.

A treasury firm selling BTC at a 40% loss while simultaneously acquiring its founder’s private assets is a combination that no amount of Bitcoin-denominated convertible note structuring can fully obscure.

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing "information gain" that cuts through market hype to find real-world blockchain utility.

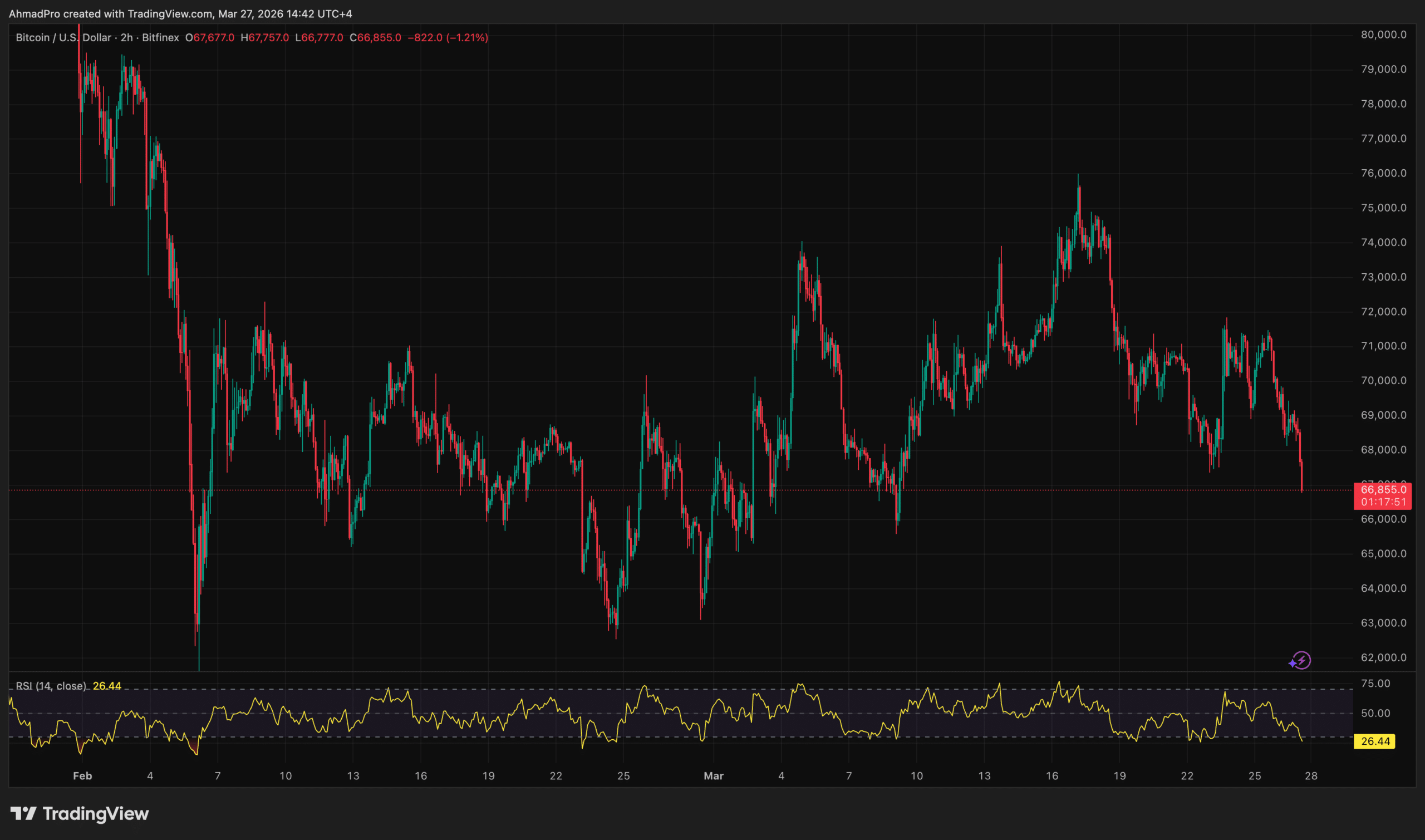

MicroStrategy (MSTR) did not add to its Bitcoin position last week, according to on-chain data and the absence of executive chairman Michael Saylor’s customary Sunday purchase signal on X – ending a 13-week buying streak that began in late December 2025.

The pause is the first break in what had become a programmatic weekly supply bid, during which the Tysons Corner, Virginia-based firm acquired approximately 90,831 BTC.

Thirteen Weeks, 90,831 BTC: What the MicroStrategy Bitcoin Streak Represented

The buying streak that ended last week was not incidental accumulation – it was a structured, capital-markets-funded acquisition program executed with near-mechanical regularity.

Beginning in late December 2025, MicroStrategy deployed capital across 13 consecutive weeks, funding Bitcoin purchases through a combination of at-the-money common stock sales, convertible note proceeds, and proceeds from its perpetual preferred equity series: STRK, STRF, and the Stretch (STRC) offering launched in early 2026.

STRATEGY $MSTR DID NOT SELL ANY SHARES AND DID NOT PURCHASE ANY BITCOIN LAST WEEK

Individual weekly purchases scaled significantly. The week of March 2–8 saw Strategy acquire 17,994 BTC at an average price of approximately $76,000, funded by $900 million in Class A common stock sales and $377 million from discounted STRC shares. The following week – March 9–15 – produced the year’s largest single-week add, marking a $1.57 billion BTC purchase. By March 23, the pace had already begun to compress: Strategy added just 1,031 BTC at a $74,326 average, a fraction of the prior two weeks’ volume.

The firm’s corporate treasury now holds 762,099 Bitcoin at an average acquisition price of $75,694 per token, representing more than 2.8% of total BTC supply. That concentration made Strategy’s weekly purchase announcement a structural event for market participants tracking liquid supply dynamics – not merely a corporate disclosure.

Without the weekly bid, one of the most consistent sources of programmatic buy-side pressure in the spot market goes quiet.

The structural explanation for the pause centers on the STRC preferred share offering. STRC was designed to raise capital for BTC purchases by attracting yield-focused retail investors – a mechanism that functions only while the shares trade at or above par. By the week ending March 23, STRC had slipped below $100, effectively closing the issuance window and removing the funding vehicle that had supported several of the streak’s larger weekly adds.

With STRC sidelined, Strategy’s residual capacity appeared limited to $76.5 million in MSTR common stock ATM sales last week – insufficient to fund a purchase of the scale that had characterized the streak’s peak weeks.

The firm simultaneously announced a new $4.2 billion STRD perpetual preferred offering carrying an 11.5% annual yield reset monthly, positioning it as what Saylor has described as the “fourth gear” of the BTC funding stack. Strategy also disclosed $2.25 billion in USD reserves covering an estimated 60–100 days of preferred dividend obligations.

Saylor addressed the pause directly, posting that “some weeks you just need to HODL” – framing the break as a deliberate hold rather than a strategic retreat. CEO Phong Le has maintained that 2026 remains a pivotal year for both the company’s capital-raising strategy and Bitcoin broadly, citing a $65 billion BTC balance despite a roughly 60% decline in MSTR shares over the prior year.

The STRC funding window closing does not cancel the accumulation plan. It pauses one gear of it.

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing "information gain" that cuts through market hype to find real-world blockchain utility.

The Senate Banking Committee is reportedly planning to hold its confirmation hearing for Federal Reserve Chair nominee Kevin Warsh as soon as the week of April 13, 2026, according to a Sunday report from Punchbowl News citing two sources familiar with the committee’s scheduling.

The timing remains contingent on Kevin Warsh completing and submitting all required disclosure paperwork to the committee – a procedural prerequisite that sources described as the primary variable keeping the date fluid. The White House formally transmitted Warsh’s dual nominations – Fed Chairman for a four-year term and Fed Governor for a 14-year term commencing February 1, 2026 – to the Senate on March 30, 2026, setting the confirmation process in motion against the hard deadline of current Chair Jerome Powell’s term expiration on May 15, 2026.

We suspect the mid-April hearing target is less a scheduling convenience than a deliberate compression of the confirmation timeline, designed to leave minimal procedural daylight between committee approval and Powell’s departure – reducing the window during which political opposition can coalesce and market uncertainty about Fed leadership can compound.

BREAKING: Kevin Warsh Fed confirmation stalled as Powell probe drags on

Kevin Warsh’s nomination is stuck in limbo as Sen. Thom Tillis blocks progress until the DOJ investigation into Jerome Powell is resolved.

The non-obvious implication is structural: a compressed confirmation timeline limits the Senate’s discovery bandwidth, which may reduce the depth of scrutiny applied to Warsh’s stated intention to pursue what he has called “regime change” in Fed interest rate and balance sheet policy – precisely the policy variables to which crypto markets are most sensitive.

Kevin Warsh: Nomination Background and Senate Confirmation Timeline

Kevin Warsh, 55, is a Stanford and Harvard Law graduate who served as a Morgan Stanley executive before joining the Bush Administration as a senior economic adviser.

President George W. Bush nominated him as a Federal Reserve Governor in 2006, making him at the time the youngest person ever to serve on the Fed’s Board of Governors. His 2006–2011 tenure included the acute phase of the 2008 financial crisis, giving him direct institutional experience with emergency liquidity facilities, balance sheet expansion, and the interagency coordination that characterized the crisis response – a résumé the White House has pointed to in characterizing him as “exceptionally well-prepared” for the top role.

President Trump announced Warsh’s nomination on January 30, 2026, following months of public speculation about a hawkish successor to Powell, whose relationship with the administration had grown visibly strained over the pace of rate normalization.

The White House’s March 30 submission to the Senate activated the Banking Committee’s jurisdiction under the Federal Reserve Act, which requires Senate confirmation for the Chair and all Board members. The committee’s hearing is the first formal public step; committee approval is followed by a full Senate floor vote, a process that in recent cycles has taken between two and six weeks, depending on floor scheduling priorities and any hold mechanisms invoked by individual senators.

BREAKING: Senator Elizabeth Warren probes Trump’s FED nominee Kevin Warsh over Epstein links.

Warsh’s name reportedly appeared on a 2010 St. Barts guest list tied to Epstein’s circle, raising questions about his past connections.

Two senators have signaled resistance. Senator Elizabeth Warren has publicly opposed the nomination on grounds of central bank independence, while Senator Thom Tillis has pledged to withhold support for any Fed nominees until the Department of Justice concludes its investigation into Powell – an inquiry the DOJ opened in January 2026 over expenses related to a multi-year renovation project at Fed office buildings.

Tillis’s procedural posture is particularly consequential because it operates independently of Warren’s ideological opposition, creating a bipartisan obstruction dynamic that complicates vote-counting for Republican Senate leadership. A majority of the Senate Banking Committee is required to advance the nomination; a simple Senate majority confirms it.

Fed Leadership and Liquidity Conditions: The Transmission Mechanism for Crypto

The crypto market’s interest in Warsh’s confirmation is not incidental – it derives directly from the mechanism by which Fed leadership shapes the liquidity environment that has historically governed Bitcoin’s medium-term price trajectory.

The transmission chain operates as follows: the Fed Chair sets the institutional tone for forward guidance, which anchors rate expectations, which determine the real yield on short-duration Treasuries, which in turn set the opportunity cost of holding non-yielding assets, including Bitcoin.

Soon, Kevin Warsh will be the first pro-Bitcoin Chairman of the Federal Reserve.pic.twitter.com/afEBrBFeWX

When real yields compress, whether through rate cuts, forward guidance softening, or balance sheet expansion, capital flows toward higher-risk, non-yielding assets as the carrying cost of holding them relative to cash equivalents declines.

Warsh’s public statements suggest a materially different policy disposition from Powell’s. In a July 2025 appearance on CNBC’s “Squawk Box,” Warsh stated that the Fed’s “hesitancy to cut rates” was “quite a mark against them,” a characterization that positions him as more receptive to easing than the current chair – or, at minimum, more willing to frame the existing stance as a policy failure.

His stated ambition for “regime change” in balance sheet management introduces additional uncertainty: if interpreted as a preference for resumed quantitative easing or a slower path of quantitative tightening, the implications for dollar liquidity are expansionary, which historically correlates with Bitcoin outperformance.

The dollar dimension compounds the effect. A Fed perceived as moving toward easier policy under political pressure – a reasonable inference from Trump’s ongoing commentary on rates – tends to weaken the dollar index (DXY), which carries an established inverse relationship with Bitcoin pricing. Markets are not waiting for confirmation; CME FedWatch data in recent sessions has already reflected incrementally elevated probability of 2026 rate cuts, partly in anticipation of a Warsh-led Fed adopting a more accommodative posture. The hearing itself may function as a pricing catalyst regardless of its outcome.

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing "information gain" that cuts through market hype to find real-world blockchain utility.

An analyst warning tied to the Digital Asset Market Clarity Act (CLARITY Act) has identified the Senate draft’s yield-restriction provisions as a structural headwind for decentralized finance tokens, arguing that ring-fencing on-chain yield distributions would directly erode the revenue models underpinning governance tokens, liquid staking derivatives, and yield aggregator protocols.

The warning arrives as the Senate Banking Committee targets a spring 2026 markup following a March 1 text deadline, with Kalshi prediction markets placing passage odds at approximately 69%. We suspect this is not a marginal concern about regulatory inconvenience – it is a warning about the foundational value accrual mechanism that distinguishes DeFi tokens from speculative instruments with no cash-flow analogue.

CLARITY Act Yield Provisions: How Ring-Fencing Would Work

The yield-restriction language at issue emerged not in the House-passed version of the CLARITY Act – which cleared the chamber on a 294-134 vote on July 17, 2025 – but in the Senate Banking Committee’s 278-page draft released January 12, 2026.

That draft introduced stablecoin yield restrictions alongside expanded Bank Secrecy Act and Anti-Money Laundering obligations for decentralized finance protocols, provisions that were absent from the House legislation and which triggered an immediate backlash from the industry.

🚨NEW: DEFI MAY NOT ESCAPE CLARITY ACT RESTRICTIONS

The proposed crypto bill may impact DeFi more than expected. Analysts at 10X Research warn token models tied to yield could face pressure.

Regulatory reach may extend into protocols and interfaces. This challenges earlier… pic.twitter.com/dGjNUlJ6tO

The mechanism functions by treating yield distributions from digital asset protocols as a regulated activity subject to the same supervisory perimeter applied to interest-bearing deposit products, effectively segregating – or ring-fencing – on-chain yield from the broader token economy.

For DeFi protocols, this is not a peripheral revenue channel. Governance tokens in protocols such as liquidity pools and automated market makers derive a substantial portion of their market value from the expectation that fee revenue will be distributed to token holders; removing or restricting that distribution severs the link between protocol utilization and token value accrual.

The House version contained a $75 million fundraising exemption, a four-year maturity timeline for digital commodities, founder trading restrictions until maturity, and self-custody rights for DeFi participants – but did not impose yield restrictions on decentralized protocol activity. We anticipate that the Senate’s insertion of yield ring-fencing represents a deliberate legislative choice to treat DeFi yield as economically equivalent to bank deposit interest, a framing with consequences that extend well beyond the stablecoin context in which the debate is usually situated.

DeFi Token Pressure: The Analyst Case Against Yield Ring-Fencing

The analyst argument, as it has taken shape in industry commentary and research circulating ahead of the Senate markup, centers on the observation that DeFi governance tokens are not equity instruments in the traditional sense – their value is substantially derived from the right to direct and receive protocol-generated cash flows. Yield ring-fencing, under the Senate Banking draft’s framing, would classify those distributions as a regulated yield product, requiring either registration or elimination of the distribution mechanism entirely.

The token categories identified as most directly exposed are governance tokens with on-chain fee distribution (where token holders receive a share of transaction fees), liquid staking tokens (where staking rewards constitute the primary yield mechanism), and yield aggregator tokens (where the protocol’s value proposition is explicitly the optimization of on-chain returns).

These are not peripheral products in the DeFi ecosystem – they represent the largest category by total value locked and the most institutionally engaged segment of decentralized markets.

🚨 CRYPTO: RIPPLE CEO SAYS COMPANY HAS NO "BIG DOG IN THIS FIGHT" ON CLARITY ACT@Ripple CEO Brad Garlinghouse said at today's FII PRIORITY Miami summit that Ripple doesn't have a major stake in the CLARITY Act battle, noting $XRP has already been recognized as a commodity by… pic.twitter.com/UGW7khu2Gj

The Senate Banking Committee’s January 14 markup postponement, which followed Coinbase Chief Executive Officer Brian Armstrong’s public criticism posted on X citing the bill’s DeFi surveillance provisions and what he characterized as a weakening of Commodity Futures Trading Commission (CFTC) authority, illustrated that the yield-restriction question has already generated sufficient political friction to stall the legislative calendar. The analytical risk is not speculative: it is already producing observable legislative delays. The risk to DeFi token valuations is not that the CLARITY Act fails – it is that it passes with the yield ring-fencing intact.

Protocol Revenue Models at Risk: Market Structure Implications

The structural parallel to the stablecoin yield debate is precise and analytically useful. The same Senate Banking draft that introduced DeFi yield restrictions also targeted stablecoin yield payments – a provision that Armstrong identified as one of four specific objections in his January statement.

The stablecoin yield question, which Senate negotiators have described as “99% resolved,” involves the same underlying regulatory logic: whether yield generated through digital asset holding or protocol participation constitutes a regulated financial product that must be supervised as such.

🚨 BREAKING: COINBASE YET AGAIN REJECTS SENATE STABLECOIN YIELD COMPROMISE

Coinbase pushes back on the latest CLARITY Act draft, warning the proposed rules could limit how stablecoin yields are structured across the industry.

For centralized players, the impact is more containable. Coinbase’s model for USDC rewards, for instance, operates within a defined legal relationship between the exchange and its users – a structure that can be adapted through registration or disclosure without dismantling the underlying product.

For DeFi protocols operating through permissionless smart contracts with no central counterparty, the adaptation path is considerably less clear. A protocol that distributes fee revenue to governance token holders on-chain has no straightforward mechanism to comply with a yield supervision regime short of disabling the distribution function entirely.

The Blockchain Association’s decision to deploy representatives across 24 Senate offices in advance of the markup – meeting with leaders from 21 firms representing 18 organizations – reflects the industry’s assessment that the DeFi provisions, not the jurisdictional SEC-CFTC allocation, are the legislation’s most commercially consequential element.

We suspect the lobbying intensity around DeFi yield is a more reliable signal of the provision’s economic stakes than any single analyst’s price target on governance tokens. The broader market structure implication is that institutional engagement with DeFi protocols will remain contingent on yield distribution clarity, and the Senate draft’s current posture provides none.

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing "information gain" that cuts through market hype to find real-world blockchain utility.

Davinci Jeremie, the Chilean software developer who became a crypto legend by urging followers to buy Bitcoin at $1, has reversed course and is now warning investors to sell their holdings.

The shift is significant precisely because of its source: Jeremie spent more than a decade as one of the asset class’s most recognizable long-term bulls, and his updated stance arrives as Bitcoin consolidates well off its October 2025 highs.

The Crypto Fear & Greed Index currently sits near 42/100, indicating Fear — a reading consistent with the broader caution that has settled over the market heading into mid-2026.

Who Is Davinci Jeremie and Why Does His Warning Matter?

Jeremie, known online as Davincij15, first purchased Bitcoin at roughly $1 per coin and went viral in May 2013 with a YouTube video titled “Bitcoin Update – just buy $1 worth of bitcoin please!”

The video, which has since accumulated 7.4 million views, was built on a straightforward asymmetric risk argument: losing a single dollar was trivial, but holding for a decade carried the potential to generate life-changing returns.

At the time of the video, Bitcoin was trading near $116.75. Those who followed his advice and held a single coin through the 2021 cycle peak near $61,000 saw returns exceeding 52,000%.

That track record is precisely what lends weight to the current Bitcoin Sell Warning he has issued. When figures associated with the 2013 cohort, individuals who rode Bitcoin from double digits to six figures — begin publicly exiting positions, it represents a meaningful psychological data point for the market. Jeremie is not a latecomer issuing a contrarian call for attention. His credibility on Bitcoin is structural, built over more than a decade of documented conviction.

Davinci Jeremie’s Sell Signal: What Triggered the Reversal?

In a recent interview with Sujal Jethwani of The Street, Jeremie outlined his current read on market structure and the forces he believes are shaping Bitcoin’s near-term trajectory. His Crypto Market Analysis centers not on technical deterioration alone but on what he characterizes as deliberate accumulation by deep-pocketed actors at the expense of retail participants.

Jeremie specifically pointed toward the influence of the Trump family, stating: “It’s clear right now the Trump family wants to push crypto down so that they can get as much as they want.” He framed this within a broader observation about time horizons, that ultra-wealthy participants operate on five-to-ten-year cycles, while most retail investors chase returns over twelve to twenty-four months.

“No, dude, it doesn’t work that way,” he said, pushing back against the expectation of rapid millionaire-making timelines.

His view is that the October 10, 2025 crash, during which Bitcoin fell from $122,000 to $105,000 in hours, liquidating over $19 billion in leveraged positions and wiping out more than 1.6 million trader accounts — was not a random deleveraging event.

Jeremie suggests it was a coordinated move by powerful players to shake out retail exposure and accumulate at lower prices. He has since expressed skepticism about near-term recovery, stating that the most likely scenario is further downside, with a best case being a return to prior all-time highs rather than a meaningful extension above them.

Notably, Jeremie has said Bitcoin at $100,000 did not excite him, a striking admission from someone who spent years forecasting exactly that kind of appreciation. That emotional flatness at a historic price level may be the clearest signal of his shifted conviction.

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing "information gain" that cuts through market hype to find real-world blockchain utility.

Approximately 80% of Strategy (MSTR) Stretch (STRC) perpetual preferred shares are held by crypto retail investors, Strategy CEO Phong Le disclosed Wednesday via social media, a figure that places mom-and-pop capital at the center of the company’s primary Bitcoin acquisition funding vehicle. The instrument has already generated over $1.2 billion in Bitcoin purchases in 2026 alone.

That retail concentration is not merely a demographic footnote. It ties STRC’s capital raise capacity directly to retail sentiment toward Bitcoin — meaning a sustained correction in BTC price can impair Strategy’s ability to fund further accumulation through the instrument, compressing the programmatic supply bid that STRC was designed to sustain.

Strategy (STRC) Crypto Investor Composition: What the 80% Retail Dominance Reveals

STRC is a variable-rate perpetual preferred share currently carrying an annualized dividend of 11.50%, paid monthly in cash, with the rate adjusted each month by no more than ±0.25% to stabilize trading near its $100 par value. The instrument trades tightly around par — closing recently at $99.94 — providing the price discipline that makes it legible to yield-seeking retail investors unfamiliar with convertible note mechanics or NAV premium dynamics.

~ 40% of $MSTR shares are owned by retail. ~ 80% of $STRC shares are owned by retail. Retail investors prefer low-volatility, high-yield digital credit.

The structure includes a holder put option at par value during unfavorable Bitcoin environments and a company-forced repurchase mechanism when conditions favor BTC appreciation. In effect, STRC functions as a digital credit instrument: the yield attracts capital, that capital funds at-the-money Bitcoin purchases, and the resulting BTC accumulation supports the broader NAV premium engine underpinning MSTR equity. Every dollar raised through STRC is destined for the order book.

In March 2026, Strategy deployed approximately $1.2 billion raised through STRC at-the-market sales to purchase Bitcoin, before switching back to common equity issuance for its most recent acquisition tranche. The two-channel capital structure — equity and preferred — gives Strategy flexibility, but STRC’s retail-heavy ownership profile introduces a variable the equity channel does not carry.

Retail-Dominated Flow: Volatility Risk and Sentiment-Driven Exits

Retail holders and institutional holders respond to drawdowns through structurally different mechanisms. Institutions operating under mandate — sovereign wealth funds, ETF products, corporate treasury programs — absorb sell-side pressure as a function of their investment policy, not sentiment. Retail holders exit when the narrative deteriorates.

Bitcoin is currently trading approximately 45% below its all-time high. In that environment, the appeal of STRC’s 11.50% yield and near-par price stability is clear: it offers Bitcoin-adjacent exposure without the mark-to-market pain of holding MSTR equity or spot BTC directly.

Speaking at the 2026 Digital Asset Summit in New York on Thursday, executive chairman Michael Saylor framed STRC explicitly as “an onramp for people who believe Bitcoin is going to be around for the long term, but they can’t handle the volatility in the near term.”

Sentiment, however, is not a mandate. A retail-dominated holder base means STRC’s secondary market liquidity and primary ATM demand are both exposed to the same behavioral trigger: a sharp BTC leg down that shakes confidence in the long-term thesis. Smart money absorbs those corrections. Retail frequently does not.

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing "information gain" that cuts through market hype to find real-world blockchain utility.

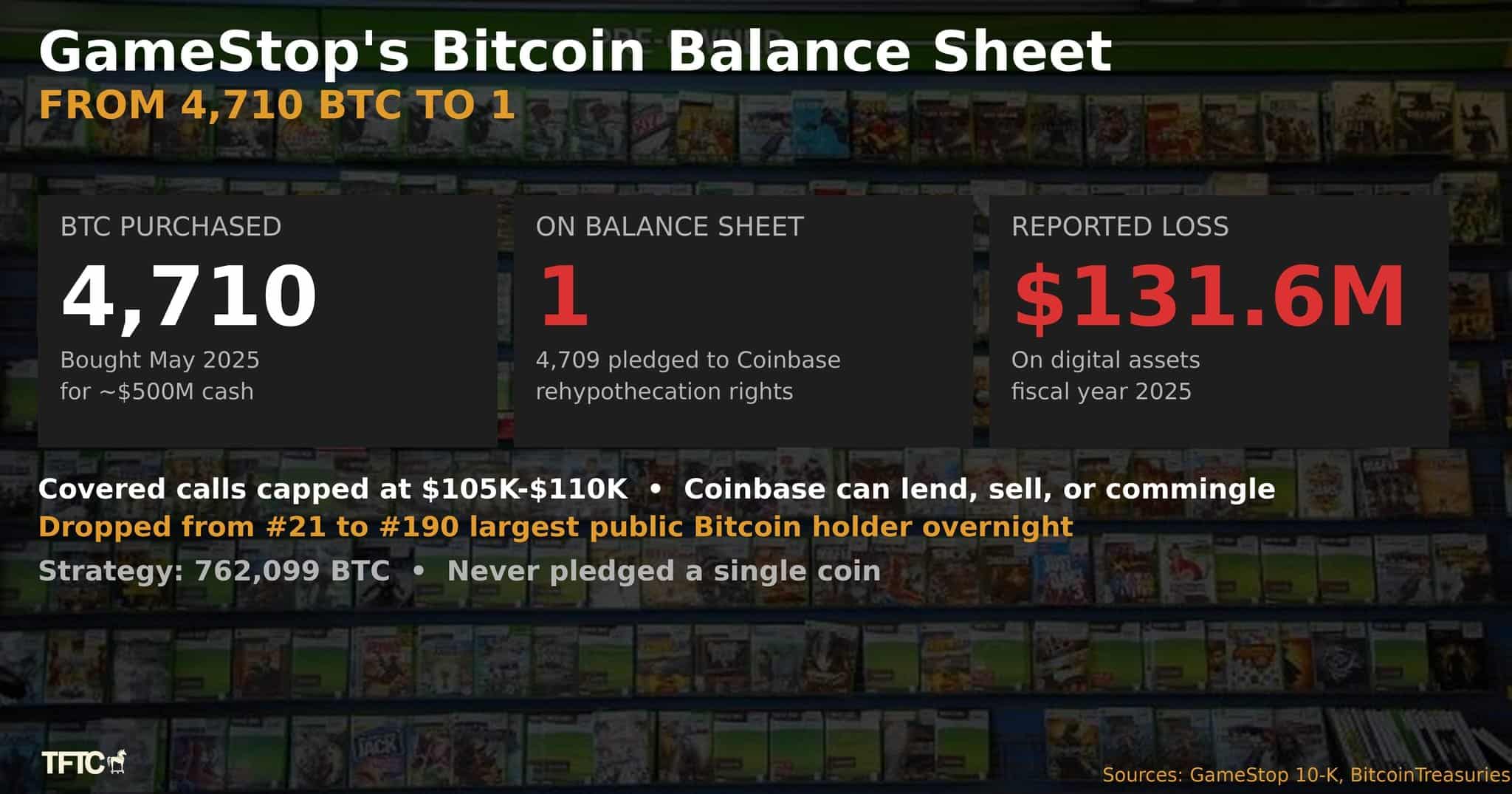

GameStop (GME) has confirmed it retained all 4,710 Bitcoin in its treasury, valued at approximately $368.4 million as of January 31, 2026, ending two months of sell-off speculation triggered by an onchain transfer to Coinbase Prime. The disclosure, contained in the company’s 10-K annual report filed Tuesday with the Securities and Exchange Commission, formally closes the overhang that had shadowed GME’s Bitcoin position since January.

GameStop Bitcoin Filing: What the Disclosure Confirms

The 10-K filing, submitted to the SEC on Tuesday, reveals that GameStop pledged 4,709 of its 4,710 BTC — 99.98% of its total holdings — as collateral on Coinbase Prime as part of a covered-call strategy executed in January. The single remaining Bitcoin sits unpledged.

The filing directly resolves speculation that erupted when onchain analysts flagged the full transfer of GameStop’s Bitcoin to Coinbase Prime as a potential precursor to liquidation.

₿ITCOIN: GAMESTOP CONVERTS $368M $BTC HOLDINGS INTO OPTIONS INCOME PLAY @GameStop's $GME $420 million bitcoin transfer earlier this year was not an exit, but it's not holding the coins anymore either.

Under the covered-call structure, GameStop sold short-dated call options with strike prices between $105,000 and $110,000, set to expire this Friday. The strategy allows GameStop to collect option premiums while retaining its Bitcoin if those contracts expire unexercised, as some already did in January. The 10-K filing records a $2.3 million unrealized gain and a $700,000 liability tied to the open options positions.

Because Coinbase Prime, as counterparty, holds the right to rehypothecate the pledged coins, GameStop derecognized the assets from its balance sheet, replacing them with a digital asset receivable. That accounting treatment, not a sale, is what caused the position to disappear from standard Bitcoin treasury rankings, pushing GameStop from 21st to 190th place in BitcoinTreasuries data. The coins were never sold.

GameStop Bitcoin Treasury: Corporate Conviction in a Legacy Retail Frame

GameStop’s board authorized Bitcoin as a treasury reserve asset in March 2025 — a decision notable partly because it came from a legacy brick-and-mortar video game retailer navigating structural decline in its core business. The move drew comparisons to Strategy’s model, though GameStop’s 4,710 BTC position is a fraction of Strategy’s holdings and was approached with considerably more caution, with the company holding steady at just over 4,700 BTC through Q3 2025 without meaningfully increasing its allocation.

The covered-call overlay suggests GameStop is treating Bitcoin not as a passive reserve but as a yield-generating asset — a more sophisticated deployment than simple buy-and-hold. That distinction matters for how the position is read by institutional analysts assessing GME as a crypto-proxy equity. GME shares are up 14% year-to-date in 2026, partly reflecting Bitcoin’s price trajectory and the clearing of the sell-off uncertainty.

The filing does not disclose GameStop’s average acquisition cost, leaving the question of mark-to-market profitability open. What it does confirm is that the board’s March 2025 conviction has not reversed.

Investors will now watch GameStop’s Q1 FY2026 earnings, expected around June 2026, for quantified covered-call income, any change to the BTC allocation, and whether the company pursues the acquisition activity that has also contributed to its year-to-date stock gains. The next filing cycle, not the current one, will determine whether GameStop’s Bitcoin strategy deepens or holds at its current cautious scale.

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing "information gain" that cuts through market hype to find real-world blockchain utility.

Coinbase has again declined to endorse the updated draft of the Digital Asset Market Clarity Act (CLARITY Act), the House-passed legislation designed to partition regulatory authority over digital assets between the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC).

The exchange’s continued opposition, most recently articulated by Chief Executive Brian Armstrong on X, comes as Senate negotiators attempt to reconcile a 278-page Banking Committee draft with competing industry priorities and White House timelines.

The refusal marks the second time Coinbase has withheld institutional support from a major legislative revision to the CLARITY Act, and it has already produced measurable legislative friction — the Senate Banking Committee postponed a scheduled markup within hours of Armstrong’s January 14, 2026, post.

We suspect the exchange’s repeated objections reflect a structural calculation rather than tactical posturing: the USDC rewards model that Coinbase operates is directly threatened by yield-restriction provisions that have survived multiple draft revisions.

CLARITY Act: Legislative Posture and Jurisdictional Stakes

The Digital Asset Market Clarity Act originated as a bipartisan effort by the House Financial Services and Agriculture Committees, introduced on May 29, 2025, and designed to resolve the long-contested question of whether digital assets should be regulated as securities under SEC authority or as commodities under the CFTC’s Commodity Exchange Act (CEA) jurisdiction. The House passed the bill on July 17, 2025, by a 294-134 margin, a vote that advanced despite Democratic objections centered on investor protection gaps.

🚨BERNSTEIN: MARKET MISREADING CLARITY ACT

Circle shares plunged nearly 21% over the last five days, dragging down broader crypto stocks.

The drop followed investor fears around a proposed ban on stablecoin yield. The concern stems from new language in the Clarity Act bill.… pic.twitter.com/qXkglh9Gi5

Senate progress stalled following a November 10, 2025, bipartisan discussion draft from Senators John Boozman (R-AR) and Cory Booker (D-NJ), and the January 2026 Senate Banking draft introduced provisions that had not appeared in the House version — among them stablecoin yield limits, tokenized equity restrictions, and new decentralized finance (DeFi) reporting requirements.

The Office of the Comptroller of the Currency (OCC) compounded the stalemate on February 25, 2026, with a 376-page GENIUS Act rulemaking proposal that would ban most third-party stablecoin yield arrangements during a 60-day comment period, aligning with banking lobby priorities but cutting against Coinbase’s product architecture.

The bill’s broader significance, establishing designated contract markets (DCMs) for crypto, clarifying custody frameworks, and resolving SEC-CFTC jurisdictional overlap, remains intact, but the accretion of contentious amendments has transformed what began as a market structure bill into a multi-front policy negotiation.

Coinbase’s Clarity Act Objections: Yield Restrictions and DeFi Surveillance

Armstrong’s January statement was direct. Posting on X, the Coinbase chief cited four specific objections: restrictions on stablecoin yield payments, limits on tokenized equity instruments, DeFi surveillance provisions, and what he characterized as a weakening of CFTC authority relative to the House-passed version. The Senate Banking Committee’s postponement of its markup in the hours that followed underscored the political weight that Coinbase’s position carries in the current legislative environment.

A bipartisan amendment by Senators Angela Alsobrooks (D-MD) and Thom Tillis (R-NC) sought to restrict stablecoin yield payments even more aggressively than the draft’s existing carve-out for loyalty programs, directly implicating Coinbase’s USDC rewards offering. Armstrong’s language — “There are too many issues” — was characteristically unhedged. Coinbase Institutional head John D’Agostino offered a more measured reading to CNBC, stating he “completely understood” why resolution was taking time, but the public posture from Armstrong set the tone.

The exchange’s position has not gone unchallenged within the industry. Andreessen Horowitz (a16z) general partner Chris Dixon posted on X that “now is the time to move the Clarity Act forward,” framing Coinbase’s withdrawal as a risk to legislative allies and the broader market structure agenda. The divergence between a16z and Coinbase reflects a genuine strategic split: firms whose revenue is less dependent on stablecoin yield products may weigh CFTC jurisdictional clarity more heavily than yield-restriction costs.

Coinbase’s repeated refusals create a measurable complication for the bill’s Senate path. Major exchanges function as de facto validators of crypto market structure legislation — their endorsement signals operational workability to lawmakers and institutional investors who lack the technical fluency to assess draft provisions independently. A bill that the largest US spot exchange has twice declined to support faces heightened scrutiny from both skeptical Democrats and Republican appropriators wary of industry opposition.

The downstream consequences for institutional market participants are significant. Without a codified SEC-CFTC jurisdictional framework, institutional capital will continue to concentrate in CFTC-regulated derivatives products listed on the Chicago Mercantile Exchange (CME), while spot markets and DeFi venues operate under enforcement-by-ambiguity. If the bill advances without Coinbase’s backing — or without revisions addressing the yield and DeFi provisions — its implementation could prove narrower in practice than the market structure clarity its sponsors advertise. Coinbase itself has estimated that implementation of a final bill would require 12 to 18 months post-passage, regardless of timing.

The March 1, 2026, White House compromise deadline on stablecoin yields, urged by Deputy Treasury Secretary Scott Bessent amid midterm election urgency, expired without resolution. President Trump’s subsequent Truth Social post conditioning legislative engagement on passage of the SAVE America Act further displaced CLARITY from the near-term Senate floor calendar.

Three specific developments warrant close monitoring in the coming weeks.

First, the OCC’s GENIUS Act rulemaking comment period, which closes around late April 2026, will establish whether third-party stablecoin yield arrangements survive into a finalized federal framework, an outcome that would either remove or harden the core objection Coinbase has raised.

Second, the Senate Banking Committee’s post-spring markup timeline will determine whether revised draft language addresses the Alsobrooks-Tillis amendment and the DeFi reporting provisions that Armstrong identified; any draft circulated before that markup will serve as a practical indicator of whether Coinbase’s objections have been incorporated.

Third, Coinbase’s own policy team has yet to indicate what specific draft language would constitute an acceptable threshold for endorsement. Until that threshold is made explicit, Senate negotiators face the structurally difficult task of drafting around an objection without a defined resolution criterion. Until the yield-restriction question is resolved — either through legislative compromise or OCC rulemaking, institutional engagement with the broader CLARITY Act framework will remain contingent, and the SEC-CFTC jurisdictional clarity the bill promises will remain deferred.

Disclaimer: Coinspeaker is committed to providing unbiased and transparent reporting. This article aims to deliver accurate and timely information but should not be taken as financial or investment advice. Since market conditions can change rapidly, we encourage you to verify information on your own and consult with a professional before making any decisions based on this content.

Daniel Frances is a technical writer and Web3 educator specializing in macroeconomics and DeFi mechanics. A crypto native since 2017, Daniel leverages his background in on-chain analytics to author evidence-based reports and deep-dive guides. He holds certifications from The Blockchain Council, and is dedicated to providing "information gain" that cuts through market hype to find real-world blockchain utility.

Strategy (MSTR) has formally outlined a plan to raise $44.1 billion in fresh capital to accelerate its Bitcoin acquisition program, signaling an aggressive counter-cyclical expansion despite the asset’s recent 40% correction from its late 2025 highs.

The initiative marks a massive escalation in the firm’s corporate treasury operations, aiming to leverage the disconnect between equity capital markets and spot asset prices to absorb floating supply at depressed valuations.

The proposed financing follows a period of heightened volatility for the asset class, yet corporate conviction appears unshaken.

By utilizing the company’s equity premium to fund spot purchases, the firm intends to continue its mandate of accreting Bitcoin per share, effectively transforming the stock into an active accumulating mechanism rather than a passive holding vehicle.

🚨NEW: STRATEGY ANNOUNCES $42B ATM PROGRAMS FOR MORE $BTC PURCHASES@Strategy has filed an 8-K announcing two simultaneous At-The-Market equity programs:

Strategy Bitcoin Capital Raise Mechanics: The Premium Engine

The core of the $44.1 billion strategy relies on the company’s ability to issue equity and convertible debt at valuations that exceed the market price of its underlying Bitcoin holdings. This Net Asset Value (NAV) premium allows Strategy to raise cash from institutional investors and deploy it into Bitcoin accretively. As long as the market values the company’s future accumulation capability higher than its current book value, the mathematical engine of the treasury strategy remains solvent.

Market observers note that this specific raise size is calibrated to maximize acquisition speed before the anticipated volatility of the mid-2026 cycle. With the capital markets remaining open to convertible offerings despite the broader crypto market downturn, the firm is effectively securing long-term funding to buy a distressed asset. This approach mirrors the “intelligent leverage” model deployment seen in previous cycles, but the scale has now shifted from mere billions to tens of billions.

The mechanism functions as a programmatic bid in the market. Every dollar raised is destined for the order book.

With $STRC under par for the whole week, the focus shifts back to $MSTR for Strategy to raise capital to buy Bitcoin.

I fully expect to see that Strategy have purchased more Bitcoin this week, but it'll be a much smaller amount compared to recent weeks.

The sheer magnitude of a $44.1 billion buy wall alters the supply dynamics of the spot market. At current market prices—hovering near $75,000 following the retrace from the $126,200 peak—capital of this size could theoretically remove over 580,000 Bitcoin from circulation. This represents a significant percentage of the liquid tradable supply, creating a scarcity shock potential that goes beyond standard ETF inflows.

Data from Capriole Investments indicates that institutional Bitcoin purchases in early 2026 have already exceeded newly mined supply by 76%. This metric aggregates corporate treasury buying with spot ETF flows, highlighting a net deficit in available coins even before Strategy deploys this fresh capital. When a single corporate entity executes purchases that outpace the daily production of the entire mining network, the programmable scarcity of the protocol is put to a stress test.

The impact is further compounded by the programmable halving cycles, which continue to reduce issuance rates every four years. With the firm recently executing a $1.57 billion Bitcoin purchase in a single week earlier this year, the pace of supply removal is accelerating toward a mathematical squeeze.

While the accumulation strategy provides a floor for demand, it introduces concentrated risk. Strategy’s aggressive use of leverage means its balance sheet is inextricably tied to Bitcoin’s price performance. A prolonged deepened bear market could theoretically pressure the convertible note obligations, though the firm has historically structured these debts with maturities far into the future to avoid liquidation cascades.

Short sellers have frequently targeted the stock during downturns, betting that the premium to NAV will collapse. However, these trades often face asymmetric risk. When Bitcoin prices reverse, the subsequent short squeeze on the equity can drive the stock price up faster than the underlying asset, fueling the premium cycle anew.

Investors should note that this $44.1 billion plan effectively leverages the entire company on a directional bet: that Bitcoin’s long-term appreciation will outpace the cost of capital required to acquire it. The infinite money glitch only works while the premium holds.

I'm struggling to wrap my head around #STRC's potential.

I know it's huge. I know it's going to continue to get bigger.

I know that for every STRC share sold, Strategy sells 3 shares of MSTR.